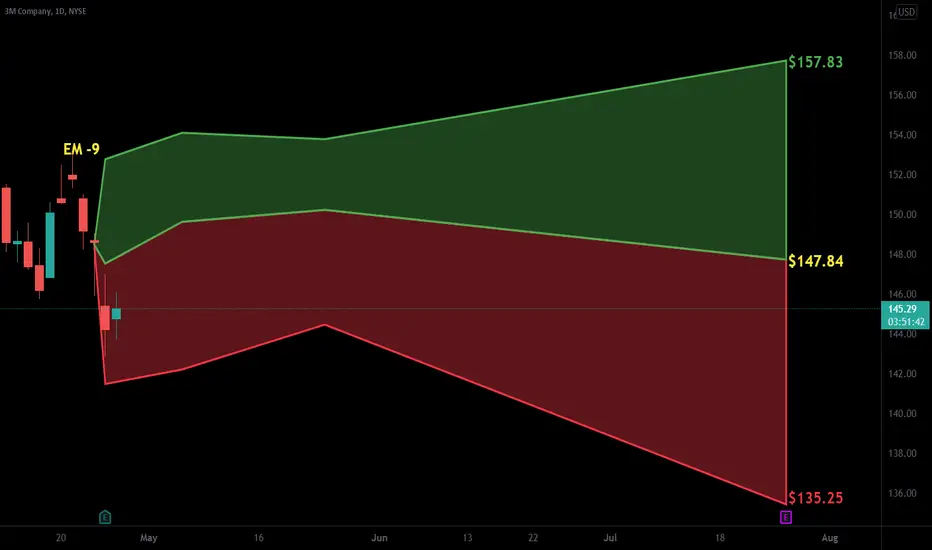

MMM - Wedge Breakdown

Rejected VMA and wedge breakdown

Price might find some buyers at the bottom of the wedge, but rollover more likely at the MAs diverge.

IF, Price can consolidate above 140, can reverse and head higher, so patience is warranted on the both sides.

MMM trade ideas

$MMM with a Neutral outlook following its earnings #Stocks The PEAD projected a Neutral outlook for $MMM after a Negative over reaction following its earnings release placing the stock in drift C with an expected accuracy of 83.33%.

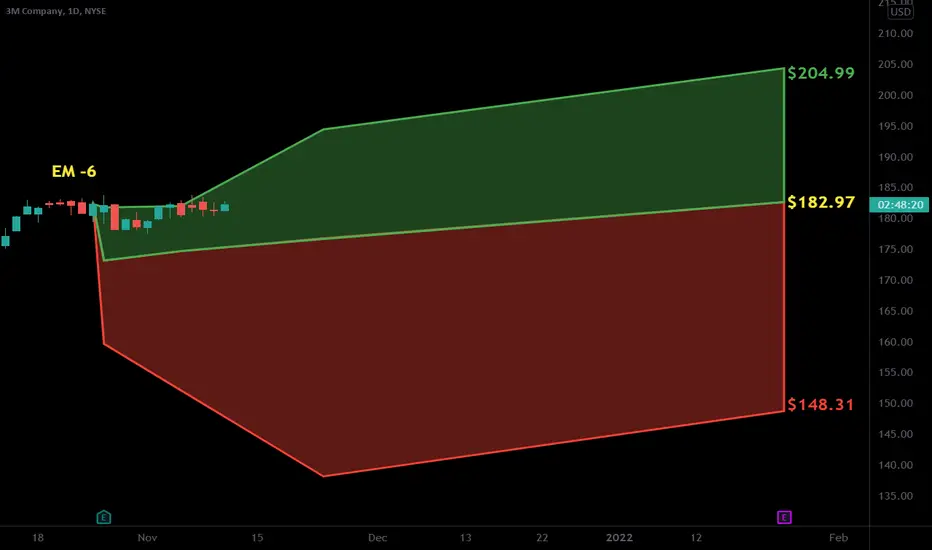

Breakout of a wedgeThe MMM.COMPANY broke the wedge and expected to continue in its downtrend until 134.70

MMM Bullish Thesis3M at the best value in 10 years, give me every share of this giant. Could certainly go lower, but will pay dividends (literally) in the future!

MMM 3M for an oversold bounceBought March 18 $147 calls. Stock is way oversold on daily and weekly technicals on a good solid company.

MMM: Oversold MMM bounced off it's 3.618 fib retracement. Look for the gap to be filled on MMM. Targets are 152-154 in the short term

Not financial advice

Time to buy!Hi everyone, Yurii Domaranskyi here. Let's take a look at the chart:

1. Price levels are working good here

2. globally downtrend

3. no report in the following 2 weeks

4. approached with a big bar

5. way down with rollbacks

6. level of a rollback

7. enough room for a move 1 to 5.1 risk/reward

8. yesterday good news "3M guides for 1%-4% sales growth in 2022, in line with estimates"

9. the price came from above

Potential risk/reward ratio = 1 to 5.1 meaning that potential risk 100$ with the possibility to make 510$

If it does make sense to you, press a thumb up! 👍

MMM - Wedge breakdownlosing all MAs on all bigger timeframes...increasing selling volume just confirms the bearishness. might find support around 156, but any bounce should be transient and selling opportunity.

mmm buy3m buy .. buy after the break and above the resistance level and 50 ma at 180.51 .. first target 192.22 .. finally target 202.00

3M | Fundamental AnalysisThe continued poor performance of 3M stock indicates that investors are beginning to lose patience with the company. At the last investor presentation, management resigned from the full-year outlook it gave at the end of October. Thus, the company's stock is even falling out of favor with value-oriented investors and increasingly evolving an option only for dividend investors.

Let's take a closer look at what's going on and whether 3M has investment potential.

In early December, MMM CEO Mike Roman and CFO Monish Patolawala spoke at the Credit Suisse Industrial Companies Conference. They immediately told investors that organic sales growth in Q4 would be in the "lower half" of the expected growth range of zero to negative 2%.

When a company lowers its sales estimates, it's never good news, but the update from 3M particularly disappointed investors. There are three reasons for this:

First, the lower sales forecast came after management raised its full-year organic sales growth forecast in late October during its Q3 earnings presentation. In the third quarter, full-year organic sales growth was between 6% and 9%, but management noticed fit to increase the lower end of the range to 8%-9%, even as the full-year profit forecast was lowered to $9.70-$9.90 from $9.70 to $10.10.

Considering that the assumed outlook for the fourth quarter has been lowered, investors are justifiably lowering earnings growth expectations. It also begs the question of why Patolawala decreased anticipations weeks after increasing them.

Second, it's no secret that investors are watching 3M's margins closely for clues as to whether its restructuring measures are bringing operational improvements. Of course, it's much harder to judge this during a pandemic, but Patolawala has previously noted the significance of volume gain to 3M's margins. Given that sales growth will be weaker than expected, 3M's margins are likely to come under even more pressure in the fourth quarter.

Third, management noted that it continues to experience supply shortages and high raw material costs. In other words, cost pressures will intensify in the fourth quarter. Consequently, 3M is seeking to raise prices so that the difference between price and raw material costs becomes margin neutral. At the conference, Patolawala was asked about pricing, to which he replied that investors should "wait and see" what prices 3M gets at the end of the quarter.

The disappointing comments about pricing and the fact that 3M has not been able to offset rising costs with pricing actions call into question the company's business model and/or ability to execute it. For the record, 3M prides itself on investing heavily in research and development to produce differentiated products that have pricing power. Unfortunately, that pricing power is not apparent right now.

Moreover, in recent years, company management has taken significant restructuring measures to improve performance. Indeed, during its third-quarter earnings call, Patolawala told investors that restructuring costs in 2021 would be between $300 million and $325 million, up from a previous forecast of $250 million to $300 million.

Moreover, 3M management has restructured the business (business groups are now managed globally rather than by country) and the healthcare segment has been restructured through multibillion-dollar acquisitions and sales.

So far, none of these restructuring actions has resulted in a noticeable improvement in growth or margins.

Still, it's hard to be too critical of a company's management during a difficult trading period. In addition, Patolawala talked about the likelihood of improvements in volume growth, pricing, lower raw material costs, and the benefits of restructuring in the future. All of these factors point to higher margins in the future.

In addition, 3M stock currently has a dividend yield of 3.5% and is well covered by free cash flow. Thus, the stock remains a good option for income-seeking investors.

Finally, it relies on your investment profile. If you're looking for a relatively safe income source, 3M stock is a useful buy. However, poor operating performance and disappointing guidance will worry investors who prefer to see evidence of progress before buying. For those investors, it makes sense to wait and see what 3M reports in its subsequent earnings releases and what margin growth is projected for 2022.

MMM Breakdown Possibility3M has been in a strong downtrend that I believe is just a long winded pullback but we're not there quite yet, right now things look bad to me, both short and long leading clouds are bearish on shorter timeframes with the long leading cloud about to change over to bearish on the weekly.

3M A good location to shortHello everyone,

Today i want to share which you my idea on 3M.

The structure of the price look verry bearish, and now the price try to bounce on the previous structure and get rejected.

So we have a good location for a short entry.

The target is on the previous support, and close to an AB CD.

For the more greedy of us, you can try to entry at 176.57

The price of 3M came out of accumulationYesterday, on a large volume, MMM jumped out of the protorgovka, which resembles the figure of an "inverted head and shoulders". Today, the price opened up with a gap.

The nearest target is 191.5 (3.8%), and ideally the maximum of the third wave (13%) should be updated.

MMM - Minnesota Money MakerDisclaimer:

1. I'm from Minnesota and still live here so I'm used to cheering for underperforming sports teams and maybe in this case an underperforming company.

2. I pretend to be able to read charts and I have never read a book on technical analysis.

3. I am not a financial advisor, in fact, I can't even balance my own budget.

4. I spent two years at ALC, as in Area Learning Center, not to be confused with the prestigious Alice Lloyd College.

5. I live in a city where 3M has poisoned the water and therefore could be suffering from brain issues due to my consumption of chemicals.

With that being said, a conservative investor may want to take a look at the support established here. It seems to me that MMM is beginning to reverse. As I see it we are looking at about 15 days to stop the spread...I mean 100 days to get to $208. If my prediction is correct we're looking at about a 13%+ return plus a .8% dividend which goes EX on 11/18. Assuming we get to that price and you decide to hold for a couple more weeks you would get another .8% div.

All of this assumes that Papa Powell doesn't make printer go burr the entire time and that President Poopie pants doesn't do anything too drastic. Supply chain issues may completely destroy this idea, but MMM being the beast that it is may just be strong enough to Hold the Line, prime, and then blast far past my prediction.

$MMM with a Neutral outlook following its earnings #Stocks The PEAD projected a Neutral outlook for $MMM after a Negative Under reaction following its earnings release placing the stock in drift D with an expected accuracy of 75%.

If you would like to see the Drift for another stock please message us. Also click on the Like Button if this was useful and follow us or join us.

MMM LongTrendline Break

At Support Zone

10/26 earning

Entry 181.2

Stop 172

Target1 202

Target2 220

Risk management is much more important than a good entry point.

The max Risk of each plan should be less than 1% of an account.

I am not a PRO trader. I trade option to test my trading plan with small cost.

$MMM | Trade IdeaNice inverse head and shoulders forming on the daily. MACD also looks like it wants to flip too. One thing to note is the potential rising wedge pattern forming after quite a large drop. (bearish)

Must wait for confirmation before considering an entry.

MMM - Bellweather, No one Rings the BellIn_Flay_Shun Trade BY the Numbers

Revenue 8.95B 24.72%

Net income 1.52B 16.69%

Diluted EPS 2.59 15.11%

Net profit margin 17.03% 6.43%

Operating income 2.05B 47.45%

Net change in cash 59M 273.53%

Cash on hand 4.7B 11.28%

Cost of revenue 4.72B 24.02%

MMM Cashing UP Reserves

Operating Margin Squeeze

NET EPS Down

COSTS UP 24%....

Bonds will not appreciate the Industrials sending LARGE WARNINGS

__________________________________________________________

Murder by Numbers - www.youtube.com

3M | Fundamental Analysis | Must Read...Industrial giant 3M will publish its Q3 earnings on Oct. 26. As always, quarterly earnings reports help shape investor thinking, whether it's near-term or long-term. Unfortunately, 3M management isn't likely to give investors much good news regarding near-term trends, but what about the long-term outlook? Here's what you should know before the earnings report comes out.

The case for buying 3M is based on the idea that the significant free cash flow (FCF) generated by the company will give management the time and strength to turn around some of the volatile performance of recent years. Furthermore, based on that very FCF, the stock looks very favorable. If the company reaches Wall Street's consensus FCF forecast of $5.7 billion in 2021, it will trade at 18.2 times its FCF (current market capitalization is $104 billion).

That's a pretty reasonable valuation for a mature industrial business proficient in increasing revenues at a rate not exceeding a single digit (in line with economic growth). If you add some margin expansion to this, and investors can expect a mix of stable earnings growth and dividend growth (current yield is 3.3%), then 3M is an excellent value investment option.

However, the question is, where is 3M's profit margin headed? Gross profit margin (profit after cost of goods) is one of the best ways to measure a company's pricing power in the marketplace. While earnings margin before interest, taxes, depreciation, and amortization (EBITDA) also includes operating expenses and is a great way to measure how well a company is managed.

3M's performance has been questionable in recent years, and this is not due to the COVID-19 pandemic.

In short, 3M needs to persuade investors that it can return the company to a long-term uptrend in margins. To that end, CEO Mike Roman restructured the business. The company is now managed from four operating segments rather than five, and business groups are now managed globally rather than by country. At the same time, management has undertaken restructuring expenses to streamline its operations.

Moreover, management has invested in digital capabilities. The poorly performing healthcare segment has been restructured through divestitures and acquisitions, such as the $6.7 billion purchase of Acelity, a trauma business, and M*Modal, a $1 billion health information systems business; both deals were completed in 2019.

So investors are right to sit back and say, "Show me margin expansion." But unfortunately, the COVID-19 pandemic has struck, and its distorting effects have made it much harder to see improvement, especially in terms of margin performance. Moreover, it is difficult to compare similar performance when the economy enters a period of downtime and resumption is impacted by soaring commodity prices and supply chain problems in key end markets.

Moreover, many of the problems associated with resumption have worsened in 2021. As a result, the critical data most investors will be watching relates to the ratio of 3M's price to its cost of production. This is a critical metric for investors because 3M management prides itself on investing in innovation to produce differentiated products - in other words, products with pricing power.

The dispute over whether 3M products are losing or gaining pricing power won't be resolved during the next earnings report, but we do know that pressure is building because of rising raw material costs and difficulties in the supply chain.

For instance, CFO Monish Patolawala projected a $0 to $0.10 decline in earnings per share at the beginning of the year due to rising raw material prices. He later raised that forecast to $0.20, then to $0.30-$0.50 in April, and then to $0.65-$0.80 in July. Moving on to the Morgan Stanley Laguna Conference in mid-September, and Patolawala guided investors to the high end of the range. And that's without taking into account the impact on the supply chain of plant shutdowns during Hurricane Ida.

Patolawala also said that inflation is outpacing 3M's ability to raise prices, and noted that auto production (a key end market for 3M) will be weaker than originally expected. In addition, the health care recovery has been uneven and the number of fee-for-service procedures is below management expectations, semiconductor shortages have impacted consumer electronics, and office resumption (3M sells office supplies) has been delayed.

All point to a troubled earnings report.

Still, much of the bad news should already be priced in, so don't be surprised if 3M stock rises if management's recommendations and comments turn out not to be so bad. Still, the earnings report is unlikely to do much good for long-term investors who are looking for convincing evidence that the turnaround attempts are working. Thus, 3M is likely to remain a good value stock, but with doubts surrounding it.

MMM. Long.I am already long and in profit. First PT is the box. Taking out 33% there and holding the rest for possible new highs.