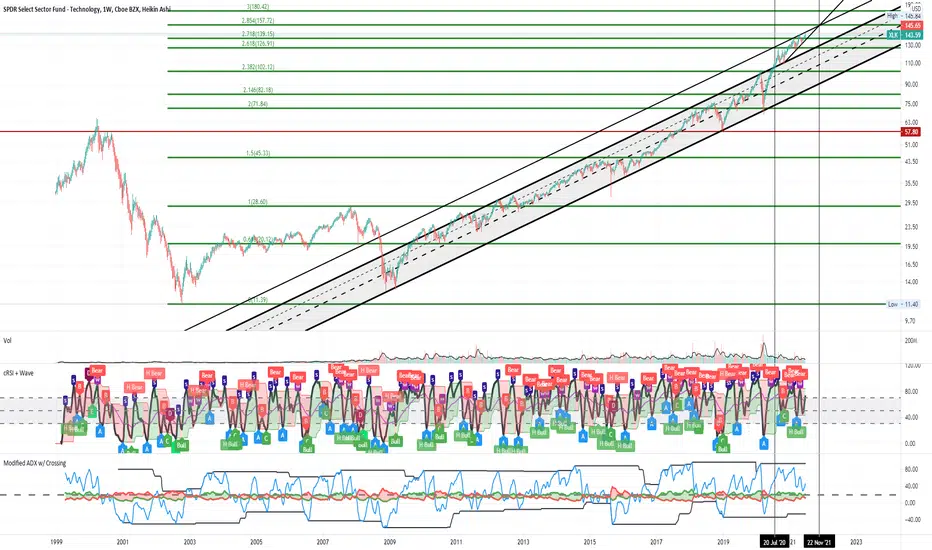

Technology overextended since July 2020 & may go until November This is about a simple as it get from a TA perspective. Tech broke the 2009 channel back and July 2020 and has not looked back since. Given its current strength and trajectory it could keep running all the way to November before we see another pullback. The air is really thin up here, but investors don't seem to care.

XLK

QQQs overbought conditions forces June SwoonQQQs has been a steadily forming this ascending triangle flag since early February as part of a 3 month corrective wave pattern (4th wave). It wont take long for this pullback to happen (June Swoon). Perhaps as early July we start to see the market bottom here around 325ish then breaking out to complete the cycle. Sometime around early to mid Sept we top out around 400ish then correct hard.

I'm still trying to figure out what can cause such a breakdown in the market. It is extremely likely that a CoVid wave hits the US once again due to the delta variant being strongly felt among young adults. I'm assuming the US will not hit herd immunity of 70% before flu season (October) and cases rise accordingly. More deaths in young adults. Some states shut down again? Who knows? The other is inflation data coming in hotter than expected and FOMC meeting in the end of Sept causes more deterioration in the market and Powell is extremely hawkish pushing the fed to raise rates sooner than expected as early as beginning of 2022 instead of end of 2022. Oof!

If both news data comes to fruition, I could see the QQQs back in the 250s. The fifth wave is complete and my count is wrong and we go back to 2015 highs. I hope only one bad data happens and we go in this long bull run in the markets for the super cycle.

Sector Winners and Losers week ending 6/18It was a volatile week in the indexes and the sector list as investors rotated on the Fed's new hawkish stance toward inflation. Energy (XLE) led early in the week, but Technology (XLK) topped the list by the end of the week, ending the week as the only sector to hold onto gains.

In second place was Consumer Discretionary (XLY). Growth stocks remained strong compared to Value stocks even in the sell-off that occurred on quadruple witching Friday.

The cyclical sectors were at the bottom of the weekly sector list, with Materials (XLB) having the worse performance among a drop in commodity prices.

Sector Winners and Losers week ending 6/11It was a mix of defensive sectors and growth stocks at the top of the sector list this week, while the cyclical sectors took a step back.

Real Estate (XLRE) led the sector list, continuing to gain on a solid housing market, higher rents, as well as a defense against potential inflation.

Health Care (XLV) also rallied this week, ending the week in second place on the sector list. Eli Lilly (LLY) helped boost the sector with news that the FDA may approve a new Alzheimer's therapy. The stock and the sector faded late in the week on the controversy over statements made by the company.

Technology (XLK) and Consumer Discretionary (XLY) were third and fourth on the list, with steady increases throughout the week as investors became more confident in the growth trade.

The cyclical stocks fell this past week. Financials (XLF) suffered from lower treasury yields, potentially impacting interest rates that drive revenue for the sector. Industrials (XLI) and Materials (XLB) declined as more of congress pushes back on Biden's infrastructure spending proposals.

Sector Winners and Losers week ending 6/4Energy (XLE) and Real Estate (XLRE) led the sector list for the week, establishing their lead early in the week. Energy got a boost from the rise in oil prices on high demand. Real Estate is gathering momentum from rising housing and rental prices while also being a great hedge against inflation.

The focus on employment data released on Friday morning is clear in two pivots. There was a sharp sell-off of most sectors except Consumer Staples (XLP) and Utilities (XLU) on Thursday ahead of the report. The two sectors are good defensive plays when investors get nervous about how the market may react to news or events.

After the report was released, Technology (XLK), Consumer Discretionary (XLY), and Communications (XLC) rallied on Friday. It seems the employment data was good enough to keep a positive outlook, while not so good to drive more fears of tapering by the Fed.

Health Care (XLV) was the worst-performing sector for the week.

XLK vs SPYTech vs Spy.. Not a good look for tech yet. While we remain under that marked line, its hard to be bullish tech overall for me. Will continue to watch.

Sector Winners and Losers week ending 5/28Growth sectors stole the show this week as investors put inflation worries aside and boosted Communications (XLC) and Technology (XLK) early in the week. The focus was on the growth sectors from Monday to Wednesday. Technology faded back in the list, buy Consumer Discretionary (XLY) joined Communications to end the week at the top of the list.

On Thursday, there was a rotation into cyclicals, bringing Industrials (XLI) higher in the list. Industrials ended the week in fourth place.

Friday brought out the defensive plays heading into a three-day weekend and the start of the summer months. That gave a boost to Real Estate (XLRE), Health Care (XLV), Utilities (XLU), and Consumer Staples (XLP). Real Estate (XLRE) ended in third place for the week, while Health Care and Utilities remained at the bottom two sectors for the week.

Sector Winners and Losers week ending 5/14It was a mix of defensive and cyclical stocks that led the sector list this week. Only three sectors ended the week with gains, while the high growth sectors took the biggest declines.

Consumer Staples (XLP) topped the list with Utilities (XLU) in fourth place. Both are defensive sectors for investors. Real Estate (XLRE) was lower in the list but still outperformed the sectors.

Financials (XLF) and Materials (XLB) joined Consumer Staples as the only sectors to end the week with gains.

Technology (XLK) and Consumer Discretionary (XLY) were at the bottom of the list. Both contain high growth companies that are likely to be impacted by inflation and potential increases in interest rates. They started to recovery on Thursday and Friday after the US Dollar and Treasury interest rates dropped.

Sector Winners and Losers week ending 5/7It was the cyclical sectors that ruled the week. Energy (XLE), Materials (XLB), Financials (XLF) and Industrials (XLI) were the top four sectors of the week.

The cyclical sectors are benefiting from a pick-up in economic activity driving demand for products from building materials, infrastructure and the manufacturing of consumables. Supply has not been able to keep up with the increased demand, driving commodity prices higher. Timber, Copper, Aluminum are all skyrocketing. And demand for oil is increasing as transportation picks back up.

While the Dow Jones Industrial average (DJI) and S&P 500 (SPX) hit new all-time records, there were four sectors that lost for the week. Technology (XLK) and Consumer Discretionary (XLY) fell on Monday thru Wednesday along with the Nasdaq, as investors rotated to re-opening and infrastructure stocks.

Real Estate (XLRE) and Utilities (XLU) were the bottom two sectors. Investors did not have interest in the defensive equity plays this week. Investors remain confident in the equities market, but are playing toward value, re-opening and infrastructure.

XLK Bullish Trade Setup XLK hourly chart showing a potential wave (C) pullback into testing the 50% retracement at 134 before we make the terminal move higher.

Sector Winners and Losers week ending 4/30Energy (XLE) led the weekly sector list for the first time since the first week of March. The sector was helped by oil prices that rose on Tuesday and Wednesday, and positive earnings reports from Exxon Mobile and Chevron.

Financials (XLF) and Communications (XLC) stocks solidified second and third place with strong opens on Thursday. Financials was boosted by positive earnings reports from Capital One and S&P Global. Communications got a big lift from Alphabet and Facebook, as advertising revenues soar amidst consumers getting back to spending.

Despite several positive earnings reports in the sector, Technology (XLK) ended the week in last place. Investor outlook appears to be that these big tech companies will not continue the same amount of growth in the next few quarters, especially compared to the previous year's numbers.

$TSLA - TESLA Stock Pennant Setting Up - Bearish immediate termTarget around $643, watch if it bounces or cracks. If cracks, then pennant will be invalidated. Eventually either a breakout or breakdown when pennant completes

XLK wave (3) Bullish XLK hourly chart showing a potential wave (3) increase into the 147 upside before a medium term corrective pullback into wave (4) sets in. One more push higher into the 147-148 and the immediate rally should take us into complete motive impulse.

QCOM (long)Nothing we have not seen before

Monday the drop to the above $135 close

i still long

I ´ve added the red slashed line to the graph

as well in purple; the MA ´s 20 blue, MA ´s 50 red, MA ´s 100 yellow

as you make your own conclusions

good luck

Charlie

QCOM QUALCOMM INC (LONG)i guessed yesterday was a good momentum, and yes that ´s worked, luck :-)

maybe $147 as short term goal ??

RSI looking good too

Maybe... anyway that ´s my bet

Invest at your own risk i have not a cristal ball, that are just ideas :-)

Good Luck

Charlie

HBAR Hedera Hashgraph 68% up??What do you think up 68%

What do you think

Let me know

Thanks

Charlie

Good luck

$NIO - STIL BEARISH, Rejected at top of channel $26 Price TargetMountain Top Formation, Rejection of Falling Channel, Could not pull through 0.618 Fib Retrace, Major Head and Shoulder