BanksLike the airline stocks, big banks have all formed similar patterns leading into Monday. Funding seems to have shifted to the banks and airlines. Many banks will be reporting earnings this coming week, including JPM, WFC, Citi (not shown) on Tues. 7/14, USB and GS Wed. 7/15, and BAC, MS, and First National Bank (not shown) Thurs. 7/16.

JPM

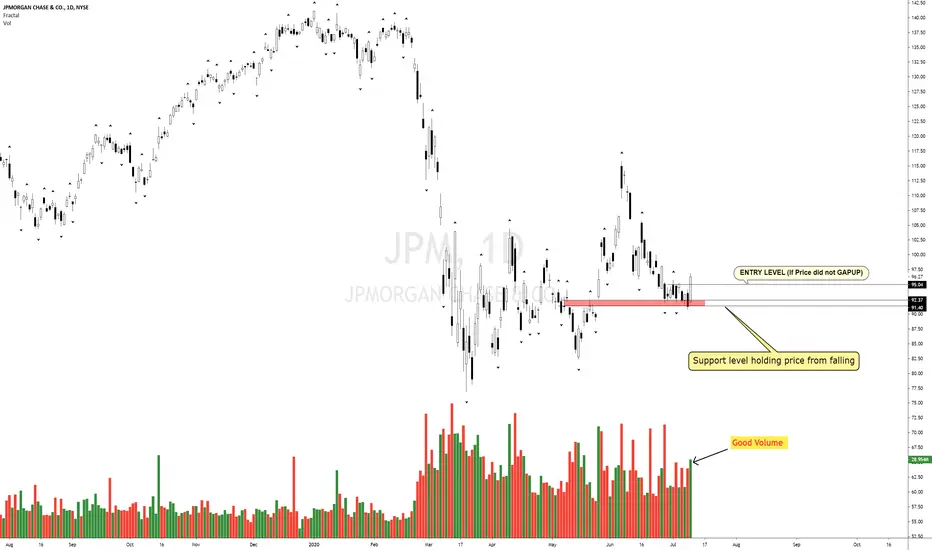

JPMORGAN STOCK PRICE COULD NOT BREAK SUPPORT AT 91.40JPM stock price has been testing the support level at 91.40 & each time the level is tested, it is met with bulls. Last week Friday bullish reversal looks phenomenon with good volume accompany the rise in price. This is the time to push the price above 100 in the coming days...

N.B

- Let emotions and sentiments work for you

-ALWAYS Use Proper Risk Management In Your Trades

$JPM Earnings playJPM like $C is breaking out of its descending triangle to the upside with RSI breaking the trend as well.

Not advise just a play I’m taking.

Please like or follow I will make more plays in coming days.

Make money!

jpmjuyl 10: first day value higher

is it real buyer or just short

covering.

Any offer below 95.15 could

lead lower as it could just

be short covering from the 107.33 area.

$C Earning playFinancials all showing similar charts descending wedge broke trend with RSI ahead of earnings. just my opinion not advise. negative market direction can make this move much less desirable IMO.

JPM Breakout for earnings?Nice bullish wedge looking formation here. There was a lot of strong buying of banks during the rally today, across the board.

No idea if the bulls are right on this one, but we'll find out really soon!

JPM back to 100basically this channel that it is in wont be held forever. once it breaks out then it is taking off for a small gain of 8. play it smart and just monitor it.

Jpm 1 hora compresionEn TL bajista con target 88,50 que deberia cumplirse hasta 2/7. Luego deberia hacer un pullback a la zona de los 97

Si el 30/6 cierra x encima de 93,70 sale de la TL.

JPM Head and Shoulders SHORTLooks like a failed retest to me. Expecting to see low 80's as early as next week.

JPM Still shorttapping the underneath of the strong trend line that has formed

rising wedge has also formed

JPM chop doesn't look goodI am long financials medium term actually but $JPM churn doesn't look good. You might be able to load up on some cheap JPM shares soon!

MARKET OVERVIEW 👨👩👧👦 | $SPY + $APPL + $JNJ + $JPM + $T📊📊📊Let's take a look at the S&P, Apple, Johnson and Johnson, and AT&T. Today we are looking to see if we can find the direction of the market going into the week by analyzing some top S&P holdings that are indicative of different key sectors.

The idea is to look at two bullish sector charts Apple (tech) and Johnson and Johnson (healthcare), and two bearish charts JP. Morgan (financials) and AT&T (communications), to see if we can find the direction of the market.

While our money is on more upside eventually (especially with Apple making an All-Time High (ATH), zero interest rates, and stimulus outweighing temporary slow recovery concerns), we want to know if the bears of the market pull us down or the bulls can sustain continued uptrend going into the week.

This write up took a long time so please Hit that 👍 button to show support for the content and help us grow 🐣

---

S&P 500 Index

Support S&P:

We have found a reaction on the S1 major price pivot point at the S/R flip. This is of course the ideal spot for the bulls to find support. If that last wick was the only test of this level we end up getting, all the better for the bulls.

If we do need to test lower levels, then the S2 untested bullish orderblock right below us provides another chance at retaining a bullish market structure.

If neither of these hold, the bulls have one last chance at the uptrend with the S3 orderblock cluster and previous range lows. A grind down to this level like we see with AT&T seems like one possible pathway there.

Resistance S&P:

The main resistance we will be looking at with most of these charts is seen in the S&P's R1 orderblock cluster at the previous swing high.

Regardless of where we find support, this resistance will be the main point of contention.

---

Apple

Support APPL:

Apple is by far the most bullish asset here. It is also the top holding of the S&P. The major support for Apple is the S1 orderblock and S/R flip cluster at the previous All-Time High. For the rest of the market to retain a bullish structure, S1 holding is key.

If S1 can't hold, the S2 orderblock and gap-fill is the next best hope for the bulls. The bulls don't want to see any weakness for Apple, so holding these levels and making new highs is key.

Resistance APPL:

Apple resembles the S&P, and that is logical because it is the biggest S&P holding. Rejection at R1 for Apple means no new ATH. Breaking R1 means a new ATH. How Apple reacts matters for the market. We see this one being broken eventually, but it has to happen sooner rather than later to lift the rest of the market up and avoid a "slow recovery."

---

Johnson & Johnson

Support JNJ:

The S1 orderblock and gap-fill on JNJ is about to be tested and is the ideal support. Finding support here means another point for the S&P bulls because we get JNJ working for us and not against us.

If S1 can't hold, we have S2 not too far away, this plays into the S&P's S2 holding as well. A dip this low isn't ideal, but the bullish market structure isn't broken if S2 holds.

Resistance JNJ:

JNJ has been correcting longer than most of the stocks on this chart. Of course, it also has a more bullish overall structure than our JPM and T bearish charts. For JNJ though, the longer correction means more levels of resistance, both the R1 S/R and orderblock and R2 S/R stand in the way for JNJ. This makes it a little harder to rely on than Apple from a pure TA perspective.

---

J.P. Morgan

Support JPM:

Big banks have their pros and cons right now, but for the market to reflect those pros S1 holding is ideal. JPM could be off to the races, or it could be making a drawn-out bottom formation.

A retest of S2 gives weight to that long drawn out bottom, therefore the big bank and S&P bulls want S1 to hold so we can maintain momentum.

Resistance JPM:

The primary resistance for J.P. Morgan is the R1 orderblock at the prior swing high. The recent market structure is similar to Apple and the S&P as a whole, it is only the previous structure that signals that JPM is a weaker asset currently. Some good JPM fundamentals could help the S&P here.

---

AT&T

Support T:

AT&T is the most bearish S&P holding we are charting. It lost its major support and is onto the S2 S/R and orderblock cluster. If this one doesn't hold, giving us a higher low, then we are simply retesting the COVID lows. If major holdings start breaking down to new lows, its a bad look for the market. The best way to avoid making new lows is not to retest old lows and instead to make lower highs. This is what the bulls want from T.

Resistance T:

Even though this is the most bearish chart, there isn't a ton of noteworthy resistance, which is a good thing. R1 is the main resistance for T. This range is notable as it was a previous resistance as well, T has this in common with the S&P... which helps confirm R1 being an important level to breach for the bulls.

---

Summary:

The S&P rallying from here or consolidating above S1 would be ideal for the bulls. For this, we need the more bullish S&P holdings like APPL and JNJ to hold their respective support levels and then rally while weaker holdings like JPM and AT&T avoid too much further correction.

If some of the weaker holdings can find support at their current ranges, or perhaps even at the next range down while the more bullish holdings stay their ground, then we could still be looking for S1 and S2 to hold for the S&P.

However, if the market tries to go bear, then we would more be looking big tech like Apple to hold up the rest of the market like Atlas while we eye S3 for support for the S&P.

It seems unlikely that we make new lows, and so we are looking for support to hold overall, but a trip down to S3 certainly will have an overall market recovery mimicking the slower recovery noted by the FED and this scenario likely results in retests of the bottom for some of the weaker S&P holdings.

Will the S&P pull an Apple and aim for new All-Time Highs, will it correct for a bit like JNJ perhaps taking us to S3, or are we going to get a JPM and T style upset? That is the question.

Resources:

www.zacks.com + www.nytimes.com

US: Major Banks in uptrend, attractive Risk RewardMajor banks in USA e.g. JPM, BAC, UBS are showing uptrend hence buying opportunities on correction

Attractive risk reward

Following entries are valid only for trading on 15 June 2020

JPM

Entry: 99.35

SL: 97.53

Target: trail the price

BAC

Entry: 24.60

SL: 24.05

Target: trail the price

USB:

Entry: 37.25

SL: 36.70

Target: trail the price

HSBC Triple Bottom Dating back to 1996 $XLF $HSBC $Bank $JPM

Why HSBC?

HSBC Triple Bottom Dating back to 1996, they got a lot of cash on their books too so fundamentally, they are worth around $26/share.

although they had shady practices n the past, if you want to pick a bank for long term investing, this is good value overall.

Entry $23 area

stoploss $20.90

1st target $24.4

2nd target $26

3rd target $32

What is Hsbc?

HSBC Holdings plc provides banking and financial products and services. The company operates through Retail Banking and Wealth Management, Commercial Banking, Global Banking and Markets, and Global Private Banking segments. The Retail Banking and Wealth Management segment offers personal banking products, such as current and savings accounts, mortgages and personal loans, credit cards, debit cards, and domestic and international payment services, as well as wealth management services, including insurance and investment products, global asset management services, and financial planning services.

$JPM Suffers the Slings and Arrows of Central Bank SpeculationJPM and other bank stocks took a hit on Wednesday when Jay Powell of the Fed noted that rates may be near zero for a long time, and other fed bankers leaked some sympathy for a negative rate path (which would ruin bank margins).

Shares of JPM could be marking the boundaries of a near-term range in the $100 area.

$JPM J.P Morgan PUT ideafirst caught my attention during the last few minutes before close. A buyer stepped up taking a $820K bet $100 Put $820K premium with a 01/15/21 expiration. Firstly I don't blame the trader/hedge because the market is in a euphoric state, while reality not so HOT.

I am looking for the $110 break tomorrow w/ $SPY selling off aggressively. This all depends on the overall market if confirms upside, will take calls.

#Daily: JPM gonna riseJPMorgan Chase & Co. CEO Jamie Dimon spoke during the Deutsche Bank Global Financial Services Conference Tuesday and argued the bank's stock is "very valuable" at current levels.

The price broke the $99,45 level. Long on retest of $99,45 or $103,11. Targets: $112,63, $125,73.

Earlier: Trump and SP500

Dare Catch A Knife? Wells Fargo.Wells is now off more than 50% since the start of the Coronavirus pandemic. However, Wells suffers from much more than a pandemic:

Over the last two years, scandals around nefarious sales practices, some unfortunate executive departures, and an inability to grow top line has hit them hard, and the crisis has hit them especially hard in revenue terms.

We're now looking at 2012 levels, not too far from where we were during the financial crisis.

Peak to trough in 2009 we saw a 69% decline in $ NYSE:WFC ... more to go here?

JPM - Potential H+S Pattern - One to Keep an eye onPotential H+S pattern on JPM, certainly one i will be keeping an eye on, as it seems that it may have started to break down from the right shoulder.

-TradingEdge

Lower rates = worse bank profitability.Hey.

I'd like to talk about the effect of lower interest rates on something called 'net interest margin'...

In other words, how banks make money.

The chart attached shows US commercial banks' net interest margin (blue) versus the target Fed Funds range (white).

Net interest margin (NIM) is a measure of the difference between the interest income generated by banks or other financial institutions and the amount of interest paid out to their lenders (for example, deposits), relative to the amount of their (interest-earning) assets.

What can we see from the chart?

As the Fed Funds target range decreases, bank net interest margin does as well.

Currently, there is talk of going negative, and just last week, Fed Funds futures priced in negative rates for the first time ever for the Dec 2020 meeting and the Jan 2021 meeting.

This is important.

See, if people are of the opinion that lower interest rates will lead to less bank profitability, then they are likely to short financial stocks.

And if people are shorting financial stocks, it can lead to a decline in lending and liquidity in the economy - which leads to dampened demand.

Over the last few years, a type of bond known as an AT1 (Co-convertible) has been used to try to sure up bank common equity tier 1 (CET1).

This gives regulators a gauge of strength of the financial institution in question.

It works like this...

The investor buys the bond, and if the share price of the bank falls to a certain level, the bond is converted into equity to prop up the CET1 of the bank.

The problem is that these investors (mainly hedgefunds and sophisticated investors), are alpha seeking...

In other words, they will hedge the delta of the decline in their bond by shorting the bank stock.

This creates a bit of a doom loop on two fronts, firstly by removing the validity of the AT1 instrument, but secondly, the decline in net interest margin leading to the shorting of bank stock and the incapability to adequately lend.

Markets and economies function on liquidity, and without it, we are in serious trouble - which explains the lengths to which governments and central banks have gone to liquify *everything*...

And why equities just keep going up...

See lower rates and more QE lead to equity risk premium compression - that is, the premium paid to take the risk of investing into higher risk assets versus simply staying invested in riskless assets (such as government bonds) - and ends up with investors piling money into equity markets.

If the perceived risk of investing into equities is a tiny bit greater than staying invested in risk-free assets, then you will get into equities.

This is exactly what has happened over the last 10 years - and it's why the market threw a fit when the Fed tried to raise back in '18.

Passive long strategies have become the norm - buying ETFs such as $SPY and simply holding - and this also affects bank profitability; less trading = less commissions paid to the dealer.

This is one reason why so many banks have moved into high frequency market making activities - Volcker prevented them from prop trading, but allows for market making (which in the high frequency trading area is largely still prop trading, although trying to prove that is tough).

Jerome Powell is expected to push back against negative rates tomorrow, and the rhetoric leading into this from Fed members has been that they do not like negative rates.

It remains to be seen, but real yields across the curve from 1y-30y are currently priced negative...

So what's the difference, really? (tongue in cheek).