OPENING: BBY MARCH 10TH 38/42/47.5/51.5 IRON CONDORBBY announces earnings tomorrow before market open, so look to put on something today before market close to take advantage of the ensuing volatility contraction. Implied volatility rank is currently at 92 over the preceding six months, with implied volatility just shy of the 50% mark.

I compared and contrasted going with my standard 20-delta iron condor, as well as a full on iron fly. Here, I'm selling the 30-delta shorts as a sort of compromise ... .

Metrics:

Probability of Profit: 57%

Max Profit: $163/contract

Max Loss/Buying Power Effect: $239/contract

Break Evens: 40.39/49.11

Delta: -2.39

Theta: 9.03

Ironcondor

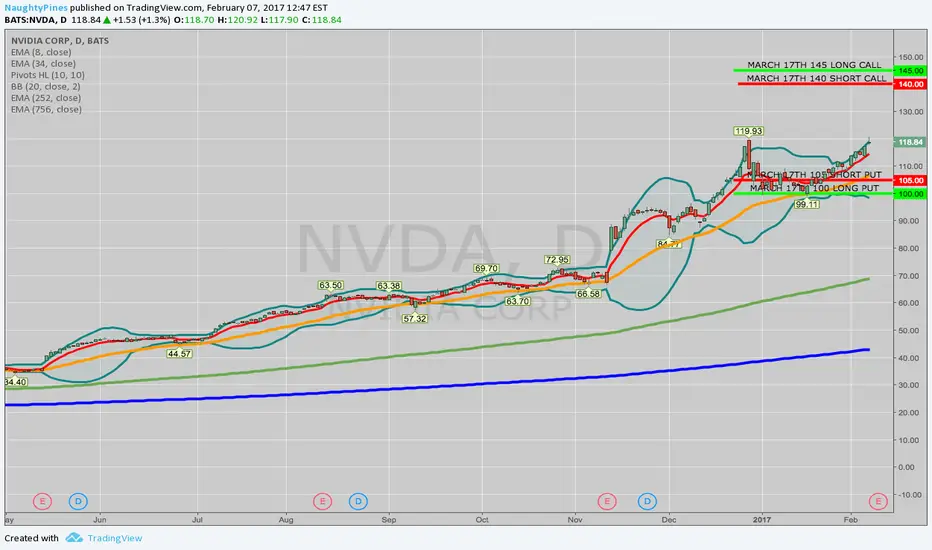

OPENING: NVDA 100/105/140/145 IRON CONDOR... for a 1.57/contract credit. (Earnings; High IVR/High IV).

I fiddled with various setups long enough ... . Here, I'm going out farther in time than I usually like to go with an earnings play in order to give myself time to be right.

Will look to manage to 50% max profit.

Metrics:

Probability of Profit: 63%

Max Profit: $157/contract

Max Loss: $343/contract

Break Evens: 103.43/141.57

TRADE IDEA: ATVI FEB 17TH 34/38.5/40/44.5 IRON CONDORATVI announces earnings tomorrow after market close, so look to put on a play in the waning hours of the NY sesh ... . Its implied volatility rank is >70%, and its background volatility is on the cusp of 50% ... .

Metrics:

Probability of Profit: 50%*

Max Profit: $231/contract

Max Loss/Buying Power Effect: $219/contract

Theta: 11.33/contract

Delta: -2.47/contract

BE's: 36.19/42.31

Notes: * -- The body of this is so narrow such that it's almost an iron fly; hence, the piss poor POP%. I considered doing the standard 20-delta iron condor here, but just couldn't squeeze out enough credit to satisfy me. I'll basically look to treat it like an iron fly, and look to take it off at 25% max profit.

OPENING: SPY APRIL 21ST 211/214/234/237 IRON CONDORI tweaked the setup a bit from yesterday, and got filled for a 1.01/contract credit.

Metrics (Currently):

Max Profit: $106/contract

Max Loss/Buying Power Effect: $194/contract

Break Evens: 212.94/235.06

Delta: -5.65/contract

Theta: .71/contract

Notes: I probably could have been a touch more patient and gone with a fill slightly above the mid. In any event, shooting for 50% max profit .... .

Basically, what I do with these is watch the position's net delta throughout its "life time" and make adjustments if necessary to delta balance (usually, rolling the "untested" side toward the "tested" side). Otherwise, I leave it alone.

TRADE IDEA: GDXJ FEB 17TH 30/36/37/45 IRON CONDOR/FLYThere isn't much non-earnings stuff out there that has both high implied volatility rank and high implied volatility. This is one of them.

Here I'm going with an extremely narrow iron condor, such that it's almost an iron fly ... .

Metrics:

Max Profit: $338/contract

Max Loss/Buying Power Effect: $462/contract

Break Evens: 32.62/40.38

Notes: I'm going to treat this as a fly for purposes of take profit and look to get 25% max.

TRADE IDEA: SPY APRIL 21ST 209/212/235/238 IRON CONDORGoing out to April for my core index exchange-traded fund position, since volatility "locally" (<45 DTE) blows here. Very close to getting 1/3rd the width of the wings; it'll have to do ... .

Metrics:

Probability of Profit: 54%

Max Profit: $92/contract

Max Loss/Buying Power Effect: $208/contract

Break Evens: 211.08/235.92

Theta: .67/contract

Delta: -5.34/contract

Notes: Here, I'm setting up my short options at the 20 delta strike, and the long options three strikes out from those. Looking to manage at 50% max profit.

OPENING: SPY MARCH 17TH 205/208/234/237 IRON CONDORI used to do a lot of SPY, IWM, QQQ, and DIA iron condors as a core position, but temporarily wandered away from those given how sporadic the implied volatility has been in these underlyings. Additionally, they have nonexistent "engagement value" (i.e., they're boring), and I haven't been able to get decent premium out of 45 day setups. Because implied volatility is so low right now, I went out to the first expiry in which I could get something approaching a 1.00 credit for a 3-wide, 20-delta setup. Here, though, I actually went a touch wider (the short options are around the 16 delta strikes).

Metrics:

Probability of Profit Percentage: 59%

P50: 75%

Max Profit: $94/contract

Max Loss/Buying Power Effect: $206/contract

Break Evens: 207.06/234.94

As with all of these, I'll look to manage the setup at 50% max profit.

OPENING: NFLX JAN 27TH 111/116/150/155 IRON CONDOR.... for a 1.21 credit.

Here are the metrics for the setup:

POP%: 69%

Max Profit: $121/contract

Max Loss/Buying Power Effect: $379/contract

BE's: 114.80/151.20

Notes: NFLX announces earnings tomorrow after market close, so I would usually put a setup on "the day of." However, I don't want to space it out, so doing it now.

OPENING: NVDA JAN 20TH 96/101/130/135 IRON CONDOR ... for a 1.09 credit. (High IVR/High IV).

Metrics:

Probability of Profit: 68%

Max Profit: $109/contract

Max Loss: $392/contract

Notes: Will look to manage at 50% max.

ROLLING: IWM DEC 16TH 116/119/121/124 IRON CONDOR ... ... to JAN 20TH 119/122/125 iron fly for a .01 net credit.

With the short put side of the Dec 16th iron condor nearing worthless and rolling intra-expiry to a fly not particularly productive, I'm rolling this out to the Jan expiry, improving the call side a strike and rolling the put side into a fly, "keeping the dream alive." Rolling is never fun, but it's the nature of the beast if you do not want to just take the loss and walk away.

This is one that will probably have to be worked a couple of cycles to get to scratch ... . IWM/RUT has just ripped brutally to the upside ... .

COVERING: IWM JAN 20TH 119/122/144/147 IRON CONDOR... for a .35 debit.

Here, I'm "cherry picking" profitable spreads from other iron condors or spreads I layered on in this expiry over time to get a combination that I can take off in profit.

The 119/122 short put vert was opened on 11/22 for a .36 credit and the 144/147 on 12/12 for a .34 credit, for a total of .70 ($70) in credits, so I'm basically taking this off at 50% max profit here.

Taking a little bit of risk off the table ... .

OPENING: LULU DEC 16TH 49/52/64/67 IRON CONDOR... for a .92 credit. Truth be told, I chased a bit. It announces earnings tomorrow after market close, but just wanted to get into play, since there isn't much premium out there to be sold, and I won't have time to putz with it tomorrow.

Here are the mid price metrics:

Probability of Profit: 61%

Max Profit: $94

Max Loss/Buying Power Effect: $206

Break Evens: 51.06/64.94

I'll look to manage this at 50% max profit on the post-earnings volatility contraction.

OPENING: IWM DEC 23RD 135/138 SHORT PUT VERTHere, I'm opening a short call vertical to pair with a short put vertical that I originally put on as a delta hedge. IWM, after all, is looking overextended, toppy here, and I want to have more short delta in place for my overall IWM position if the election "exuberance" begins to wear thin.

I filled the spread for a .52 ($52)/contract credit and will look to take off the now complete iron condor as a unit at 50% max profit if I get the chance.

Notes: I generally don't leg into iron condors as a matter of course, but it just so happened that I had more "put side" units than "call side" units. This balances that out.

ROLLING: IWM DEC 9TH 116.5/119.5/123.5/126.5 IRON CONDOR ... ... to Dec 9th 124/127/127/131 Iron Fly for a .47 ($47)/contract credit.

I figured I had to do something here to improve the prospects of this broken iron condor.

I first rolled the short call vert side from the 116.5/119.5 short call vert to the 127/131. The only way to get a credit from this intra-expiry roll was to widen the spread by one strike.

And then rolled the short put side up to the 124/127, creating an iron fly.

In order for this setup to have a "perfect finish," price will have to roll back into the "body" of the setup toward expiry. If it doesn't, I'll roll the short call side out again, improve the strikes if I can, and sell the short put side against for a credit such that the cost of the roll is "net credit."

Just can't believe that IWM won't give up some of this post-election up-move ... at some point.

GAP StrategySince HLF is oversold , there's a very good oportunity in making money. Target is 57.00 , but I belive that it will go over 60 .

MARKET HOURS:

Good oportunity for STRADDLE (in case the price wiil be between 59 and 63) after the market opens, as well as IRON CONDOR (STRANGLE seems to be ***too risky***).

SPY DEC Iron CondorThe IVR is high in SPY. The VIX is trending up slightly. Either way I like how wide I've gotten my strikes, so I've sold this IC.

Now it's just a waiting game for days to pass and theta to come off.

OPENING: IWM DEC 16TH 103/106/121/124 IRON CONDORWith VIX still "up there," I'm putting on a bit more premium selling setups in broad market instruments.

Metrics:

Probability of Profit: 61%

Max Profit: $104/contract

Max Loss/Buying Power Effect: $201

Break Evens: 105.01/121.99

Notes: I'll look to manage this at 50% max profit. I would also note that this is doubling as a bit of delta hedge for an IWM position I already have on that was beginning to skew delta positive. This setup is slightly delta negative and brings my net delta for my IWM positions to slightly negative (which is the way I generally like things).

OPENING: IWM DEC 9TH 108/111/123.5/126.5 IRON CONDORI slapped this one on rather hastily on Friday with the FBI "reopening-Clinton-email-investigation" volatility pop we had on Friday.

Unfortunately, I didn't get what I usually look for in these setups -- a credit of at least 1/3rd the width of the wings (I got it filled for .89 ($89) per contract), but could have done slightly better if I'd not been in such a hurry (looks like you could get .92 ($92) at the mid at the moment) (63% probability of profit; $92/contract max profit; $208/contract max loss/buying power effect; break evens at 110.08/124.42; delta -5.87).

I'll look to manage it at 50% max profit.

EARNINGS: JNPR, GRPN, AND TWTR (DIRECTIONAL PLAYS)A couple of other ideas for next week surrounding earnings ... . I like to have a lot of these ideas in the hopper so that I can price setups during regular market hours; some of these aren't as "sexy"/liquid during NY as they appear in off hours.

JNPR Dec 2nd 21 short puts; .45 cr at the mid (strike around long-term support). Earnings (10/25). I generally do these earnings plays with a short strangle or iron condor, but just can't get squat out of one of these strats in JNPR, so might as go directional.

TWTR Dec 16th 15 short puts; .60 at the mid (I'm more fixated on the 14 strike, since it's around long-term support). If I get a dip post earnings (10/27) that "juices up" the 14, I'll pull the trigger on that. Roll, roll, roll until a buyout rumor or until a buyout actually occurs. If it pops higher, I shrug my shoulders and say, "You doofus. You waited too long." TWTR has good metrics for my standard short strangle or iron condor, but I'm fixated on going directional here with the repetitively resurfacing buy out rumors which may, at some point in time, result in an actual buy out ... .

GRPN: Dec 16th 4.5 short puts: .31 at the mid. Earnings 10/26. That shortie is quite close into current price in the scheme of things, so this one would be a crap shoot. Either it takes off to the upside or look forward to getting put the stock at 4.5 (minus the credit you received on the front end). The good thing is that background IV is always fairly high, which would help with selling calls against.

TRADE IDEA: EWW DEC 2ND 43.5/46.5/53.5/56.5 IRON CONDORWith a 52-week implied volatility rank of 100 and an implied volatility of 35, EWW -- the Mexican ETF, beckons for premium selling ... . Here, the iron condor brackets the ZigZag/Donchian channel indicated support/resistance at 48.22 and 54.25 nicely, with break evens for the setup above and below those marks.

Here are the metrics for the setup:

Probability of Profit: Unavailable*

Max Profit: $100/contract

Max Loss: $200/contract

Break Evens: 45.50/54.50

Notes: * -- Accurate probability of profit metrics are unavailable here in the off hours, probably due to after hours bid/ask in the underlying showing bid 44.12/ask 73.00/last 49.98. Look to manage at 50% max profit.

THE WEEK OF 10/16: WHAT I'M LOOKING ATWhile I grind away on various covered call positions (I only have one covered call with an October short call on; the rest are in November or December), I'm looking ahead to some decent earnings for premium selling.

Generally, I'm looking for underlyings whose implied volatility is above the 70th percentile for the past 52 weeks and that have background implied volatility of greater than 50% to play for a contraction in volatility immediately following the earnings announcement, with the go-to strategies being short strangles or iron condors.

Currently, there are four underlyings with good liquidity options that announce earnings next week and whose volatility is above the 60th percentile for the preceding 52 weeks: IBM, NFLX, UA, and EBAY. I'm screening for >60 implied volatility rank at this point, since volatility in these could still ramp up to my >70%, meaning that they might be worth keeping an eye on.

IBM -- Announces 10/17 after market close. The implied volatility rank is now in the 85th percentile. Unfortunately, the background implied volatility is far from being up to snuff at this point for me (28.3%).

NFLX -- Announces 10/17 after market close. Implied vol rank: 64th percentile; implied volatility 56.6%. It's very nearly "there". Hopefully implied volatility pops a little more right before earnings.

UA -- Announces 10/17 after market close. Rank: 62; implied vol 41.7%. Needs more.

EBAY -- Announces 10/19 after market close. Rank: 93; implied vol 41.6%. Needs more.

After I look at implied volatility percentile and the background implied volatility, I look at what I can get out of a setup. Generally, I'm shooting for a 1.00 credit for either a short strangle or iron condor, since I look to take these off at 50% max profit (i.e., a .50 ($50)/contract profit). Alternatively, I look at whether a short straddle or iron fly would make sense if the underlying is just too cheap to yield a decent enough credit. With short straddles/iron flies, I generally look to get 2.00 in credit at the outset, since I tend to manage those at 25% max.

TRADE IDEA: XLU NOV 18TH 42/47/47/52 IRON "FLY"I haven't done many of these in the past, but I'm beginning to warm up to them, particular with instruments that wouldn't ordinarily yield jack diddly squat with a traditional iron condor setup.

Here's how this iron fly compares to an iron condor with similar break evens (it would be a Nov 18th 43/46/48/51):*

Probability of Profit: Fly: 52% Condor: 52%

Max Profit: Fly: $220 Condor: $120

Max Loss: Fly: $280 Condor: $180

Break Evens: Same

Theta: Fly: 1.85/day Condor: 1.32/day

Take Profit: Fly: 25% of max ($55 profit) Condor: 50% of max ($60)

Spread "Repair": Same for both setups; roll tested side out for duration and, if feasible, away from current price for strike improvement; sell the oppositional spread against for a credit that exceeds what it cost to roll the tested side. Taking into account all credits received and debits paid, shoot to take off the rolled setup at the original take profit.

As you can see, the probability of profit is the same for setups with the same or substantial similar break evens, and there's little meaningful difference between the profit I would get if I managed the fly like a short straddle (at 25% max) and the condor like a short strangle (at 50% max) ($55 vs. $60).

The research I have looked at for short straddles and short strangles indicates that short straddles reach 25% max in about 30 days on average; short strangles 50% max in about 25 days, www.tastytrade.com (short strangles); tastytradenetwork.squarespace.com (short straddles), which appears to suggest that there is no huge difference in "time to same profit" for the two strategies. (Although those studies involved short straddles and short strangles, you can think of iron flies as "defined risk short straddles" and short strangles as "defined risk short strangles"). Consequently, even though you're receiving greater credit up front for the iron fly, you're probably going to have to wait around for it to reach 25% max profit about the same amount of time as you would an iron fly.

The important takeaway here is that -- but for the iron fly -- I would probably not put on a defined risk trade in XLU. The reward is too small; the risk too great in comparison. So, another tool in the tool box for when you just can't enough credit out of a play in an instrument with your "regular" set of tools ... .

* -- Generally speaking, I would not set up an iron condor this tightly. I'd set up the short option strikes at the edge of the expected move and then the long options out from there 3-5 strikes (e.g., a Nov 18th 42/45/49/52). However, that particular setup would only yield a .72 ($72) credit/contract, and -- were I to manage that trade for 50% of profit -- would only yield .36 ($36) for a setup with a max loss of 2.28/contract ($228). The type of setup for an instrument with these particular metrics (price, implied volatility, etc.) is generally not worth it, in my opinion.

TRADE IDEA: IWM OCT 21ST 112/116/126/130 IRON CONDORWith VIX finally breaking 15 here, I need to strike while the iron is hot ... . The instrument of choice -- IWM, the broad index exchange-traded fund (as compared to SPY, DIA, QQQ) with the highest implied volatility currently ... .

Metrics:

Probability of Profit: 52%

Max Profit: $127/contract

Max Loss/Buying Power Effect: $273/contract

Break Evens: 114.73/127.27

Notes: Naturally, I'm going to watch the markets early next week to see if there's continuation in this dip. If there is, I may hold off slapping something on for even higher volatility. Heck, I waited eight weeks or so for VIX to break 15; I can wait a little longer if it's going to go higher ... . The natural alternative to this setup would be RUT with similar strikes -- i.e., 1120/1160/1260/1300 ... .