USDJPY Tanks after Dovish FOMC MinutesThe FOMC minutes had an extremely dovish tone today. This will further boost the selloff in USD across all majors. Particularly notable is USDJPY, and EURUSD. Both Kovach Momentum Indicators are solidly bearish, and the price action continues to push the lower band of the Kovach Reversals Indicator. Sell any rallies in USD.

If you like the Kovach Momentum Indicators, or Reversals Indicator, sign up for access at quantguy.net!

Macroeconomic Analysis And Trading Ideas

FOMC Minutes Reveal Inflation Still a ConcernThe FOMC minutes are being released as I write this, but weak inflation seems to one of their key concerns. Expect the yield curve to continue to flatten as this gets priced into the long end. The spread between the US 30 year and Us 2 year has been careening off a cliff lately and given this news, it is safe to expect this trend to continue. The Kovach Chande indicator is solidly bearish, confirming this, and the lower bound of the Kovach Reversals indicator is continuously being pushed.

If you want access to the Kovach Momentum Indicators, Reversals Indicator, or Crypto Specific Indicators, please sign up at quantguy.net!

Yield Curve Below 1%, Racing to the BottomThe yield curve (spread between the 30 year and 2 year spread) just broke below 1%. All indicators suggest this trend to continue. It has been encroaching the lower Bollinger Band of the Kovach Reversals Indicator, with no retracement in sight. A retracement will be confirmed by a green triangle, if an when it happens. The Federal reserve should be very mindful of this in their December meeting.

If you're interested in the Kovach Reversals Indicator and more, sign up for access at quantguy.net!

Bitcoin will beat the Central Banks (Sarcasm) // If you honestly believe cryptos growth wasn't anything other than to bring forth a cashless society governed by the world banks / you thought they just would go down without a fight... I hope u truly start "reading the history books"

But hey, don't listen to me, go all in and don't forget to also invest in those 1300 not at all similar crypto coins. Bubbles need fuel & stupidity to survive... Just know that it prob won't go as you thought it would at the end.

Those who are in power are not giving away anything for free ;)

If you're one of those early investors in Bitcoin... Gosh... take profits quick and allocate that nice ROI into where the money will flow once QT starts messing with the market //

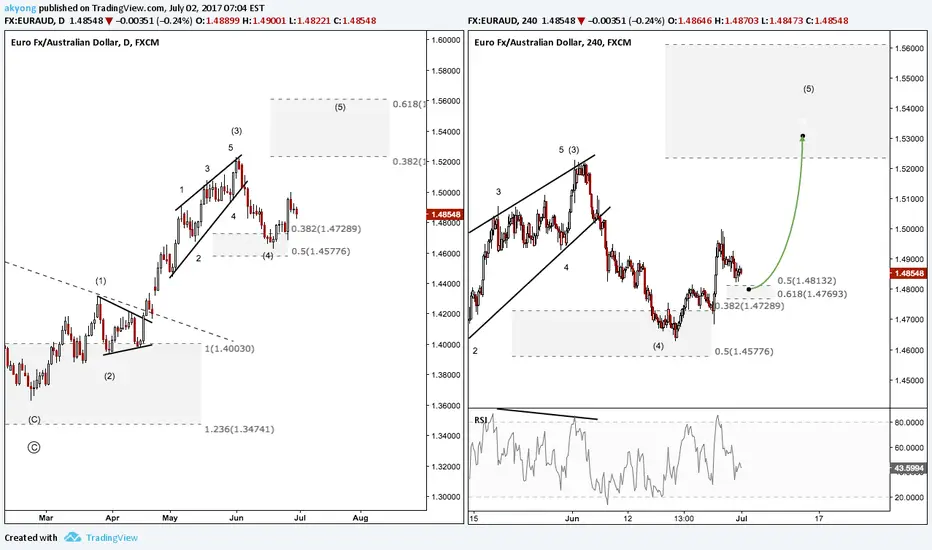

EURAUD - Time to head higher?Early June we shared an idea on EURAUD short term downside towards 1.4732 area ().

After hitting that area and completing the short term correction, we are now expecting price to move higher towards 1.5230 area to complete the overall 5-wave structure.

Here are some reasons for me to have a bullish bias on EURAUD -

1) Price development on daily timeframe is showing a potential 5-wave structure development;

2) Price is currently showing bullish impulses on 4-hour timeframe after hitting the 0.382 - 0.50 fibonacci area, completing the minimum retracement for a wave 4 correction; and

3) The most recent price move is corrective, thus indicating that there is a high probability of seeing a bullish impulse to the upside.

*Next week RBA Rate Statement and Cash Rate might be the catalyst to move the Aussie.

P.S. My personal bias is to the upside, but doesn't mean it's time now to take a buy trade. Make sure you have a proper strategy to engage the trade according to your personal plan :)

It´s The Politics. Stop Following Technical Analysis ...

U.S. investors brace for mounting political risks as they decode Trump

Quote: Barry James built up his $4 billion mutual fund largely by studying balance sheets, earnings and market share. In the last few weeks, however, he has realized that he must look at a new force in the market: U.S. President Donald Trump.

Trump's unpredictable governing style and stated desire to renegotiate trade agreements and punish companies that seek out lower-cost forms of labor are upending the classic notion of fundamental investing, said James, who manages the James Balanced Golden Rainbow fund.

Source: www.investing.com

Kiwi CPI data and RBNZ Gov Wheeler preview/fundamental analysisThis is a daily NZD/USD chart. Later today we have key New Zealand Q4 CPI data and comments from RBNZ Governor Wheeler. Both releases are likely to provide volatility so it would be wise to cover open positions and avoid opening positions around the time of the data and speech (21:45 GMT and 23:00 GMT). Data from New Zealand has been mostly positive since the last rate decision in November where the RBNZ cut rates to a record low 1.50%. Since then, Q3 GDP came in better than expected, and although the prior was revised lower from 0.9% to 0.7%, bullish pressure was observed in NZD. Alongside this the most recent jobs data was beat expectations. We can expect the both the CPI data and RBNZ speech to be encouraging, given the recent positive data as well as Goldman Sachs and Bank of New Zealand stating they see RBNZ hiking rates this year. Wheeler's most recent comments also suggest he sees solid CPI data as he stated the economy is performing relatively well and inflation is to return to preferred range by Q4 (which is 1-3%). With all that said, and the simple fact that New Zealand interest rates are so low, we can expect this data to at least be in line with expectations, possibly even come in better and possibly bullish price action for Kiwi Dollar, but always be wary of manipulation!

FOMC / Educational Preperation. XXX / USD # USD / XXXHello guys.

Personally I am excited as we get closer to FOMC, and I will be trading FOMC event.

I will have positions on:

DXY

USD/JPY

GOLD

SILVER

EUR/USD

I will manage to trade this event with High Frequency news trading machine, as HFT is back in da building, and we had a great success trading news with this machine. Last NFP was sweet as well.

Since I have a lot of new followers that have no Idea how HFT works, I will refresh memory for you guys as well write down things for new followers, but always remember News Trading involves high risk.

So basically what we are doing is predicting the first momentum with HFT.

If you remember the last NFP, you saw the momentum spike upwards. Strange even tho we printed good NFP and rate data, still first momentum was up, and HFT nailed it's job.

Persoanlly how I trade news with HFT is I open BIG lot size, and set TP for this trade to lock the profits, if TP not hit I monitor situation manually and if momentum loses STEAM I close the trade.

I am not using SL because in first second or second before the news there are spikes before momentum direction and spike size depends on your broker.

Last NFP for example It was not a killer, because I feel the signal that is being generated and I know whether the event will be meh.. or event will have strong impact.

Last NFP generated weak signal and we got relatively weak NFP impact.

The same goes for FOMC, as I will feel whether the event will be weak, or strong impact based on data that I get.

But I reckon that FOMC will be a TURNAROUND event and not a Dirrect one.

Basically what that means is that HFT will generate for example LONG signal, once FOMC come out the momentum will be LONG ( spike up ) and then the turnaround follows, the same vice versa.

Of course it can be dirrect move and if signal for example is LONG it can start to go long, and go straight up, same vice versa.

Anyway I'll be in the trade, because this FOMC event should be great and should move the market and you can trade any xxx/usd usd/xxx pair if you want since on all of them there will be an impact.

Let me know in comment section below if you have any questions.

TPP

Longterm view on GoldPretty self explanatory, shaded areas are where I think price will turn, based on unfilled orders existing right outside those candles.

I'm particularly convinced by Jim Rickards(youtu.be), who argues that gold will go through a severe re-pricing whenever the relentless expansion of central bank balance sheets overwhelms the low-yield, deflation-biased economy we're currently in. QE/Stimulus does not work (currently ECB/JCB have been buying ~$200b worth of stuff EVERY MONTH) and all that misspent capital will have to be accounted for one way or another, ultimately through inflation. We're going to experience an inflationary episode much like the 70's when the dollar depegged from gold and the world became pure fiat, except the paradigm shift this time around is for permanent money creation to become the norm, aka helicopter money, which arguably is a more sensible form of money (read here: en.wikipedia.org(1860s_money)). When the debts placed upon us become monetized by the very central banks they originate from, it will be known that deflation is dead, and there will be nothing stopping inflation from taking over and reclaiming all that misspent capital. Now is a risky time to go long general bonds/equities, focus on preserving wealth rather than chasing yield. %5-10 in physically owned gold makes fine sense as insurance against severe market, rare as their occurrences may be, and the price currently seems quite fair.

Gold made a drastic climb up from 1050 to 1250, assuming 1050 is a reliable floor the worst we'll see for gold going forward is probably the 1090-1120 range. Although, it's totally possible the ComEx paper market gets slammed for whatever reason, if they are that bold then I don't really expect anything worse than 900. If you buy physical gold you shouldn't have any plans to sell it for at least three years.

BUY USD DIPS VS GBP/ NZD: DOVISH FED W. DUDLEY SPEECH HIGHLIGHTSFed Dudley was speaking At A joint New York Fed, Indonesian Central Bank Seminar On Sunday evening when he left a mixed impression for the markets to digest - saying "it is premature to rule out an interest-rate increase this year" but then on the contrary saying "Raising Rates Prematurely Would Be Riskier Than Moving Slightly Too Late" and following up that sentiment with "Investor Expectations For Flatter Path Of U.S. Interest Rates Seems 'Broadly Appropriate'" and pointing out the medium-term risks are seen skewed to the downside - all of which somewhat contradictory expecting a 2016 rate hike.

IMO these comments are more less positive news for the greenback, given the hawkish July Minutes should take precedent (despite the market weirdly selling the september hike being officially put on the table) and after the DXY lost every day last week I think it will struggle to continue this trend into this week as the drop in rate hike expectations/ fed funds rates should flatten out - Likely seeing the bulk of the dovish expectations price last week - september 25bps hike expectations fell from 25% at the beginning of the week to 12% on Friday following the miss GDP report - will likely bottom out around here to 8%min.

That said, given the BOJ's miss we could easily see further pressure on US rates this week as imo the failed big stimulus hopes are likely to fade the risk-on environment of late, and move us back into the safe haven trend that has dominated 2016 - so dont be surprised to see some more risk-off rate expectation USD selling/ bond buying - look out for consecutive moves higher in UST or moves lower in tnx.

In the medium term this still hasnt changed my view of bullish USD and at present IMO this selling wave has opened up the opp for some good USD buying entry points e.g. kiwi above 0.72, stelring at 1.33, and eur at 1.115 - kiwi and sterling the best trades as we move into RBA, BOE and RBNZ within the next 10 days which should realise considerable downside for kiwi and cable (and for those trading aussie too, tho i prefer the kiwi proxy).

Fed Dudley Speech Highlights:

-Fed's Dudley Warns It Is Premature To Rule Out an Interest-Rate Increase This Year

-Dudley Says Fed-Funds Futures Prices Seem 'Too Complacent'

-Dudley Says There Is 'Room For Improvement' in Fed Communications, But They Are Growing More Transparent

-Dudley Says His Baseline Outlook For U.S. Growth, Inflation 'Has Not Changed Much In Recent Months'

-Dudley Expects 2% Annualized U.S. Growth Over Next 18 Months

-Fed's Dudley Says Medium-Term Risks To Economy Are 'Somewhat Skewed To The Down Side'

-Dudley Says Brexit Impact Has Been Short Lived, But Longer Term Potential Fallout 'Hard To Gauge'

-Dudley Says Fed Takes Dollar Appreciation Into Consideration, But Not Targeting Any Set Exchange Value

-Dudley Says Evidence Accumulating The Crisis-Era Headwinds 'Are Likely To Prove More Persistent'

-Fed's Dudley Warns it is Premature to Rule out an Interest-Rate Increase This Year

-Dudley: Investor Expectations For Flatter Path Of U.S. Interest Rates Seems 'Broadly Appropriate'

-Dudley Says Raising Rates Prematurely Would Be Riskier Than Moving Slightly Too Late

SPX: BOJ MISS = BULL RUN END +2% + 2016 SAFE HAVEN TREND RESUMESEnd of the bull run

Global Equity Indexes:

1. SPX/ Global Equity indexes in the past 2/3wks saw a post-brexit central bank easing induced rally, as many CB released dovish statements following the vote which spurred investor confidence in fresh easing.

- IMO much of the bull run was based on BOJ easing hopes, given the size of the economy (4th largest) stimulus from the BOJ had risk sentiment increasing affects - though now in light of no new easing from the BOJ and many CBs shrugging off/ UK internalising the brexit impacts I believe this bull run is over.

2. Technically speaking we may see another week or two of sideways or +1% as the market awaits easing policy information from the BOE (6th largest economy), but past this and regardless of what the BOE does i think the upside bias will cease. BOE is only likely to inject 50bn over probably 6m+ which is a drop in the ocean relatively as the BOJ does 100bn+ in one month, so by mid august latest I expect risk-markets to turn sour and a 10% correction is likely.

Confirmation the risk-rally is over:

- During this bull run we have seen risk markets/ SPX make gains rather frigidly, one day up one day down has been the trend - rather than the usual breakout green green green rallies of the past - this to me indicated that the topside was cautious and reinforced my view that it was central bank driven (not equity market performance driven). Thus, Confirmation of the trend turning to risk-off will be consecutive days of risk markets falling (SPX/ global indexes) OR consecutive safe haven markets rising (Gold, UST, Yen) and the emergence of a strong negative correlation between the two assets will be a solid second indicator that the 2016 risk-off trend is back.

Trading Strategy - a number of ways to play this one:

1. Short FTSE100 @6700 or 7000 (wait for BOE) - this is my favourite trade but has a few conditions. We have built some resistance at the 6700-800 level so here isn't a bad place to sell however i think we will get a better selling vantage point next week, assuming the BOE cut the bank rate 25bps.

- The BOE easing should move FTSE100 up 3-4% in a few days into the 7000 ATH key level as easing boosts business conditions and a lower GBP increases FTSE company international competitiveness. The 7000 level is where I am aiming for FTSE shorts with sell-limit orders as 1) its all time high levels; 2) I like to fade central bank action since it is artifical; 3) the broader risk-run is over so FTSE will suffer with the rest of the market

2. Short US Indexes @Market - SPX is perhaps the best short ATM given it trades right at its newly set all time high levels and on the backdrop of the BOJ miss we should see some downside soon.

3. Long Yen @mrkt - in the immediate term my favourite trade I like long Yen (for 200-400pips) against USD and GBP, given the BOJ backdrop is most related to JPY markets. We have already we seen the risk-off transmission taking place in here as Nikkei sold off 2% after the result and JPY grew 3% but i still think in the immediate term e.g. 1wk we can see more JPY topside and Nikkei weakness - me prefering to trade the FX strength over the equity as the equity often follows as a function of FX strength.

4. Long Bonds or Gold @mrkt - for the medium/ longer term I like buying govt debt, particularly UK gilts (BOE QE increases demand) or Gold - Gold we saw move higher on Friday in reaction to the BOJ so it will be interesting to see if we can get risk-off confirmation run from this next week (look for 3/4 green days).

Risks to the view:

1. US Earnings have outperformed imo on average this Q, so the risk-run may be sustained for longer than the 2wk window that I expect. Nonetheless, i think even this is capped at 4wks e.g. we should be in full bear mode by the start of September - look out for the confirmation, a run of 3/4+ days of consecutive safe haven gains is often all the markets have to signal to show

GBPJPY: BOJ MISS; BOE HIT? MORE SELLING ON THE HORIZONBOJ Miss:

1. BOJ deliver one of the biggest misses in history (vs expectations/ pressure) - only increasing ETF purchases and dollar funding by apprx $60bn annual in total vs 10-20bps of Depo and LSP cuts + 5-20trn in QE increase + ETF increase.

*See attached post for in-depth detail on the BOJ situation and price action history/ Yen strength/ Safe havens*

BOJ Miss Compounded with a BOE Hit:

1. BOE are expected to ease by 25bps and possibly add 50bn to their QE programme on Thursday - a BOJ miss combined with a BOJ hit should cause compounded losses for GBPJPY as there are two drivers - Yen should continue this week to get stronger (as BOJ easing expectations surpass and Yen strength increases) whilst GBP gets weaker as the BOE on Thursday likely takes action, reducing the value of Sterling - with both providing the optimal environment for downside.

- Historically, when BOJ has delivered new policy/ missed GBPJPY has sold off aggressively between 2-8days and 700-1200pips. Now whilst I dont expect the same level of aggression in the near-term as the relative value is much lower now (135 vs 175) so moves lower should be smaller - I do expect that 400pips lower on the day is not the end of the selling rally for GBPJPY.

- Initially at the start of the week i expect GBPJPY to move lower at least another day (satisfying historical moves), perhaps into the 133.5 level which would be 550pips, lower than the smallest sell-off but fair given the relative value changes - not that i would be surprised to see more.

- Later into the week is when I expect the bulk of GBPJPY losses to come (e.g. Thurs/ Fri) - the reason for this is as 1) any Yen downside risk from the MOF releasing upside in the details of their stimulus package would have surpassed e.g. increased stimulus from 28trn-40trn (unlikely) or increased govt spending section - both of which devaluing yen moving gbpjpy potentially higher. Though I think the risks are more skewed to MOF delivering a package that strengthens JPY as it undershoots expectations as several MOF members have mentioned the package being over several years - the more years the less punch the package has (given some expected it (5% of gdp) to be spent in 1yr), equally the less direct govt spending portion of the package will also lessen the depreciative impact on yen (rumoured to be 13trn, if less then Yen could get considerably stronger). As mentioned I see the MOF release to be asymmetrically skewed to expectation downside for these reasons.

2) BOE GBP selling pressure would happen when they cut the rate and adjust their QE programme - this is a highly likely scenario as BOE MPC Minutes in July said "Most members expect to loosen policy in August" and recently the BOE's biggest hawk M. Weale switched stance in light of UK Business PMI/ Optimism prints at 10yr lows saying the BOE needs to act fast/ delaying policy further doesn't make sense.

Trading strategy: Sell GBPJPY @mrkt 133.5TP1 130.5TP2 128.5TP3 - risk averse traders could wait for the 50-60% MOF/ general Vol bounce into 136-38 level before shorting - I would reshort here anyway.

LONG USDJPY: ANOTHER BOJ OUTPERFORM CASE - 28TRN GOVT STIMULUSAnother argument for the BOJ outperform case - Post BOJ Buy $Yen @MRKT 111tp:

1. We know BOJ and JPY Govt Abe/ Aso have had many meetings post-brexit and as it follows the JPY Govt have announced today that they will deliver a fiscal stimulus package of 28trn - which was to the very right of the curve (10-30 was talked about).

- This in mind, imo it is rational to extrapolate that 1) surely if the JPY govt are choosing a tail end stimulus package (aggressive), BOJ will be inclined to do also? Given that it is the BOJ remit for economic targets like inflation, not the governments - BOJ wouldnt want to be seen as dropping the egg would they e.g. govt does as much as it can but BOJ only midly eases - doesnt make sense? Especially given the relationship between kuroda/ aso/ abe it would almost be impossible.

- 2) The BOJ will know/ see that the JPY Govt are taking the "extreme" side of measures, so once again this puts the BOJ under-pressure to do the same as they dont want to be seen as "letting the side down" especially as it is the BOJ who really has the power to change things - the Fiscal package is rather an indicative/ nice gesture of the govts willingness to help - rather than any real hard easing when you consider the Govt package is likely to be 28trn a year but the BOJ purchases/ injects 80trn A MONTH to its monetary based in JGBs - thats 960trn a year. So 27trn govt vs 960trn BOJ - is the govt really making an impact or are they instead signalling their commitment/ putting pressure on the BOJ? I think so.

Under-performance case:

1. Perhaps less meaty, but nonetheless a valid point - Japan, JPY Govt and BOJ have lived with low inflation/ deflation for the past several decades and no "extreme" action has been taken to resolve it (well not enough to fix the problem anyway) so this pressure on the BOJ we talk about above - is it real? or is it a theoretical pressure that they "Must" hit their targets?

- If history predicts the future then yes, it is a theoretical economic pressure - they haven't hit the target for 20yrs so why would they do measures to hit it now? There's no public pressure, im sure theyre happy consuming at lower prices - unlike with high unemployment.

- Off topic but it would be interesting to see a Japan with high Unemployment - an economic indicator that causes civil unrest (Greece riots) and is a necessity to be solved for the wellbeing of any nation - thus my bets are if unemployment was at 15-20% (similar comparison to deflation) for the past 15yrs something drastic WOULD have been done a long time ago, or be done on Friday to fix it. After all, theres no driver to fix something that doesnt really need fixing is there? Think about the last time you went to extreme measures to fix something that wasn't much of an issue...

Fed preview: What to expect of EUR/USD?EUR/USD pair is trading around 1.10 handle a few hours away from the FOMC rate decision.

No one expects the Fed to hike rates today, but experts believe the Fed is way behind the curve and is under pressure to acknowledge the improvement in the data. Marc Ostwald, Strategist at ADMISI discussed Fed preview in detail on our Finance show today. The show is available on youtube here – www.youtube.com

Experts are right in stating that actually there is no valid reason for the Fed to hold back. In my view, record high stock markets are screaming rate hike. But it is unlikely the Fed may move today.

Coming back to EUR/USD, a neutral FOMC would be a non-event for the markets. If Fed drops rate hike hint, the pair could head lower to sub 1.09 levels. On the other hand, a dovish talk (very low probability) could push the pair higher towards 1.1080 levels.

Now let us look at what the chart has to say

Daily chart has classic bearish structures –

Rising trend line breached

Falling channel established

Bearish symmetrical breakout inside falling channel

If charts are to be believed, the one must be ready for a hawkish FOMC statement!

ECB - wait & watch mode, Draghi could talk down EuroDraghi takes center stage 45 minutes after the European Central Bank releases its latest monetary policy statement later today. Almost no one in the markets expect the ECB to move rates today. London city experts on our today’s London open finance show are quite confident that ECB would remain on a wait and watch mode, while Draghi as usual may make an attempt to talk down the Euro. (The link to today’s Finance show titled “ Market Roundup: ECB’s next move depends on what BoE does - TipTV - www.youtube.com )

No reason for the ECB to move rates or expand asset purchase program as -

Bond yields are at record lows, 10-yr German bund yield is negative

World has not come to an end after Brexit vote. There is no evidence yet of a significant deterioration in the economy

Financial markets are doing well; US stocks are at record highs

China published upbeat Q2 GDP and monthly retail sales, industrial production figure

Oil prices are steady

Draghi would want to watch BOE and BOJ’s next move

Draghi would want to watch what the Bank of England does in August and act accordingly – Is the message that comes through from today’s Finance show.

The only big difference in the post Brexit world is that – earlier ECB had to keep an a eye on BOJ, now after Brexit ECB would have to keep an eye on BOJ and BOE.

Markets put the probability of a BOE rate cut in August at 63%. Meanwhile, a double barreled (fiscal + monetary) stimulus is expected from Japan. Whether or not BOE and BOJ/Japanese government deliver is a different debate. But for now Draghi would want to wait on the sidelines.

We may see minor tweak to the asset purchase program like – drop in the threshold for bond purchases and/or extending the maturity of asset purchase program. However, these moves are unlikely to result in a major sell-off in the common currency.

Draghi could push dovish button via comments on the post Brexit world and situation in Italian banks and European banks at large.

EUR/USD – Play the trend line

From technical perspective, the EUR/USD pair is heading into the ECB event on a weaker footing, courtesy of bearish price action as discussed here - EUR/USD prepared for a break below 1.10 and here - EUR/USD eyes 1.0940

As of now, the pair is back above the falling trend line seen on the hourly chart, but is having a tough time holding above 1.1033 (23.6% of 1.1428-1.0911).

Euro’s failure to sustain above 1.1033 followed by a break below yesterday’s low of 1.0981 could yield a quick fire drop to 1.0937 (61.8% of 1.0517-1.1616) – 1.0911 (Brexit day low).

On the higher end, we need a daily closing above 1.1088 to signal short-term bearish invalidation.

Another view on ECB and monetary policy impact on FX markets worth watching - www.youtube.com

SELL AUDUSD - JUNE RBA MINUTES HIGHLIGHTS - DOVISH/ CUT POSSIBLEOn the margin RBA remained in line with previous meetings, adding little but still keeping it on the dovish side imo. Once again, as in previous minutes (and from several other central banks) RBA continued to communicate the necessity of "watching key data" to drive future policy decisions. Interestingly though, they also mentioned the negative impact of a strong AUD which in turn supports RBA doves out there as a cut is the remedy to stop a deflationairy currency in its tracks. Further, RBA notably were under no illusions regarding their inflation situation stating " inflation set to stay low for some time" - another encouraging stimulus for doves given inflation's important position/ weight for setting future policy.

As per the attached post, i remain dovish/ bearsh on aussie$, and i continue to expect a cut to 1.50% (25bps) this year given i expect their inflation to remain stagnant. Clear targets are 0.73 when probability of a cut is higher - though i would enter shorts regardless if AUD$ could find its way to its 12m highs at 0.78, though unlikely.

I like USD strength in the medium term too hence supporting the short Aussie dollar view

RBA Minutes Highlights:

RBA MINUTES: BOARD TO WATCH KEY DATA, WILL MAKE ADJUSTMENT TO RATES IF NEEDED; REVIEW OF FORECASTS IN AUG WILL HELP STEER POLICY

- Inflation set to stay low for some time, employment mixed, retail sales look set to pick up

- Stronger AUD would complicate economic rebalancing

- Economic transition is now well advanced

LONG USD VS JPY, EUR, GBP: HAWISK FED BULLARD - FED FUNDS RALLYBullard is the lone Fed official forecasting just one additional rate increase, and expects modest growth over the next two and a half years. But he reiterated Tuesday he's not expecting the economy to head south. However, did go out of his way to mention a relatively dovish point "We Have Some Ammunition if We Need it During Next Recession". Nonetheless he remained hawkish net on the margin, reiterating FED Georges hawkish comments regarding the labour market "About as Good as It's Ever Been", whilst using the June NFP print to flatten any questions regarding the low May print saying "Strong June Jobs Gains Showed May Report Was 'An Anomaly'". Similarly Bullard continued with Georges sentiment of the US's post-brexit robustness stating that the "Market Reaction to Brexit Shock Was 'Satisfactory,' 'Orderly'" - and infact surprisingly pushed this hawkish brexit sentiment on to new levels of "Ultimately the Brexit Impact on U.S. Economy Will be 'Close to Zero'". This is perhaps the most hawkish/ upbeat statement i have heard form a key Fed member since the decision which is positive given Bullard's naturally dovish stance.

Bullard also stressed the need for a solid US Fiscal package to boost demand, where i have to say fiscal stimulus has almost gone forgotten about in the last 7-years post crash, given the dominance of the central banks, quoting "U.S. Badly Needs Fiscal Agenda for Boosting Economic Growth".

Once again todays "FED speaker tracker" continues to add to my long $ view in the medium term. Today already we have seen front end rates continue their aggressive recovery this week, with the fed funds rate implied 25bps hike probability now trading for Sept/ Nov at a whopping 18% vs 11.7%Mon, with Dec trading at 36.3% vs 29.2%Mon .

10y UST (TNX) rates trade up another 4% today after a 5% gain yesterday, whilst 30yrs trade 3% up on the day (TNY) - as global risk rallies. Whilst USD is trading a little weaker in the immediate term as it readjusts lower for risk-on USD selling, long USD/ DXY is my medium term view as we continue to see the US FOMC Rate curve aggressively steepen, which is likely to continue for the next week at least - steeper implied curve means hike is more likely - more likely or realised hikes = increased (in the medium-term) dollar strength. Further, we expect dovish/ easing BOJ BOE ECB over the same period, this monetary policy divergence compounds the long $ view against its 3 biggest crosses (hence the long DXY expression)

Medium term trading strategy:

1. The best expression of this medium term USD view is long DXY - as above I hold 8/10 conviction views for a number of the heavily weighted USD basket crosses based largely on likely monetary policy divergence in the medium term (FOMC Hiking whilst BOE, BOJ & ECB ease/ cut) e.g. LONG USDJPY @104 - 106.3TP1 109.5TP2; SHORT EURUSD @1.11 - 109.3TP1 107.5TP2; GBPUSD @1.34 - 131.2TP1 128.5TP2

BUY USDJPY @104 & SELL GBPUSD @1.33: RISK-ON, POLITICS, BOJ, BOEThe Federal Reserve's regulatory point man said work to address the lessons of the 2008 financial crisis won't be complete without better regulation of short-term funding both inside and outside the banking system.

St Louis Fed President Jim Bullard may be the Fed's new super dove, but he's no pessimist, he says. Bullard is the lone Fed official forecasting just one additional rate increase, and expects modest growth over the next two and a half years. But he reiterated Tuesday he's not expecting the economy to head south.

Trading Strategy

1. Given this I remain bullish on the $ in the medium term, despite this spike in risk-on which IMO is unlikely to last more than 2wks. In the immediate term I like long $yen as the best play ATM vs other expressions - with a target of 109, entry at 104 as 1) the markets have finally signalled they are ready for a recovery bull run, post the brexit risk-off/ safe haven rally - largley on the back of CB stimulus. I believe USDJPY has been the most sold risk-on asset, thus it is now ripe for buying; 2) JPY fiscal stimulus is likely to come; 3) BOJ is likely to deliver 10-20bps of cuts to its interest rate 4) we have broken the 104 "brexit seller resistance level" which has held since the vote - this break imo means we can now move to 109+ as the recovery leg before resuming lower; 5) the Fed Funds Rate curve continues to steepen across the curve but particularly aggressively in the front end (yesterday 10ys adding 5%) and as a result implied probabilities of hikes continue to rally across the 2016/17 tenors (Dec hike now 33.7% vs 29.2%Mon); 5) check the attached posts for long $jpy support

2. Secondly, short GBP$ is a trade i am closely eyeing.. I am a 70% seller at 1.32 (90% at 1.35) - short GBP rallies is the preferred trade as the BOE is likely to deliver easing in Aug that will drive us down to the 1.25 terminal rate that I have predicted - thus i am hoping we get some "poor information money" flows into GBP up to 1.34/5 going into Friday as 1) UK Political Uncertainty is eased - as Theresa May is the New PM starting Wednesday; 2) GBP buying on Thursday if the BOE doesn't cut rates, whilst I (and the market) believes an august cut is the likelihood instead, given the aggressive GBP selling these past weeks it is prudent to assume quite a large amount of money may/was be betting on a July Cut thus if this "disappoints" some of the market we could see cable trade higher to 1.34+; 3) Long GBP is the risk-on trade, so if risk holds up/ carries on rallying we could see GBP$ take us to 1.34+ - CB and Fiscal stimulus + the fact risk has been depressed for so long, i believe risk has the momentum to rally until the end of the week at least (next risk-rally then looks to 28th July for BOJ stimulus?)

3. The long $Yen and short GBP$ also acts as a dynamic hedge as the long UJ is the risk-on coverage, with the short cable the risk-off half - combining both semi-hedges your exposure, something i like to do when trading.

FED Tarullo Speech Highlights

- "the conditions for destructive runs that threaten financial stability could exist even where no institutions that might be perceived as too-big-to-fail are immediately involved"

FED Bullard Speech Highlights

- Bullard: An unemployment rate around 4.7%, gross domestic product growth of 2% and the Fed' preferred inflation gauge, the personal consumption expenditures index, at 2%.

- "If there are no major shocks to the economy, this situation could be sustained over a forecasting horizon of two and a half years"

- "we have no reason to forecast a recession given the current state of the US economy"

RISK ON/ OFF PARADOX CORRECTION - SHORT SPX/ FTSE & USDJPY P2 Post Brexit SPX vs USDJPY

1. One had expected risk to sell off post brexit as global uncertainty increases, given the amount of volatility in the FX markets in the lead up, this was the rational expectation (whilst VIX traded subdued). However, instead, SPX recovered 6% whilst Yen also rallied 7% higher in the days following the vote.

2. This risk-on risk-off positive correlation rally is almost unseen in markets (especially not at the 75% correlation level) as JPY and SPX positively correlate for the first time in 4 years (as below).

3. As discussed previously this is either 1) because markets are unusually evenly split on sentiment, going against herd behaviour with the marco outlook trading as a non-consensus between participants; 2) CBs have given risk an artificial boost based on supportive statements/ measures.

Trade the paradox

1. Short FTSE100 @6600-6800 resistance with a 5700TP (January lows) - once artificial BOE easing rally is finished, likely near 66-800 FTSE will plummet in the medium term as 1) This underlying risk-off bias which has gone un-priced as yet (safe havens up 21% in 2016) prices - not to mention reaching near ATHs, with 10y resistance.; 2) brexit (still not priced in equities)/ Political uncertainty drags on economy and stocks - especially financials, which has a knock-on effect of corp credit tightening; 3) this structural CNH deval prices and hits UK export stocks as it did in Jan

2. Short SPX @2100 with a 1985TP - SPX at these levels looks an attractive short 1) as discussed CNH depreciation which is a macro issue for all stock Exporters to China (biggest market/ growth market) hasnt priced any revenue downside yet like they did in January (-8-13% previously). 2) underlying risk-off bias is still yet to reprice risk lower (2016 safe havens up 21% av. Gold 28%) + only 2% away from ATH - favourable short lvls; 3) Earnings sell-off likely around the corner as investors derisk/ hedge against "shocks"; 4) Brexit induced CB easing/ dovish rally likely to fade soon as it isnt structural growth and FOMC rates are recovering in the back-end (Dec Hike looms). SPX has a more conservative target vs FTSE as less brexit downside & its a structurally stronger index with growth stocks

3. Id also suggest dynamically hedging these positions with 1) Long high growth and low China revenue individual stocks e.g. Goog, FB and/ or 2) shorting GBP index or a GBP cross , lower GBP hedges any potential BOE easing rallies that the FTSE short may negative experience, and also short GBP is a solid trade to have regardless of any FTSE risk you have on the table.

*See part 1 for more information "RISK-ON RISK-OFF POSITIVE CORRELATION? SPX VS GOLD, JPY & UST P1"

BUY $YEN @ 107 PRICE & SD VOL RESISTANCE LEVEL$Yen dropped 150 pips following the $ employment report and I for one am confused...

I had assumed JPY had been acting as a Risk-Off function against the FED hike e,g, $yen had been falling to these levels as the fed hiking risk caused safety flows into JPY... turns out this may not be the case.

The market has absorbed the emp report at dovish, UJ shedding 150 pips, i actually expected JPY to weaken on a bad $ report as i expected risk-off money flows (that had been giving the jpy strength) to leave the yen as the chance of a hike in june is reduced and people looked to take more risk.

The reaction we got was actually the opposite, the market priced the poor NFP like every other CCY, and USD weakened..

The play from here imp is still the same though, I still like buying USD against the JPY as monetary policy divergence is strife and JPY just seems to be expensive atm.

JPY is even more expensive now that the probability of a fed hike is reduced, so there should be less "risk off" money in the ccy.

I will engage in my long JPY at the support level of 107, where both price and 2SD volatility provide a high probability of a retracement back up.

Buy limits placed at 107.050, 106.9, 106.4 106.2 - Spread risk out incase of further downside - bet on the idea NOT the single price