ZN - 10 Year Note Futures / An important ChartThe importance of ZN as an Instrument cannot be overstated.

It has been extremely technical and Reliable in assisting us in

forecasting Rate Mid Curve and provided the ROC's for TNX.

Today's MAcro Data begins with the CPI @ 8:30 AM EST using

the new Base Effect from the BLS.

______________________________________________________

CPI is projected to be 4%.

Food prices have already increased substantially into 2022

as we indicated Mid-Q4 2021 - Pordiucer were going to begin

passing along increases at an average rate of 20-23%.

Energy continues to Rise as do Commodities, on balance, across

the Board.

M2 continues to move higher, as does the Fed's Balance Sheet.

_______________________________________________________

The reaction to the CPI this morning will provide direction for the

Indexes the balance of the week.

Pricing Power is being passed along to end-users (consumers) at

a time when the Federal Reserve is indicating they are about to begin

an aggressive reduction in Liquidity and an accelerated pace of

increases to the Fed Funds Rate.

We have seen back to back ALGO driven increases in the ES / NQ / YM

and indicated 10 Yr Yields would pullback ~ 1.81% (1.808 was close

enough).

2021/2022 measured move is now .998 to 1.808 - a near doubling of

the Mid Curve.

________________________________________________________

The Bond "safety" Trade wasn't entirely wrong until the Curve

began to work its magic. We indicated in July Rates would begin

rising again into the end of 2021.

Where the Bond Buters lost sight of the Safety Trade was quite

simple - Convention holds only when the Yield Curve is steepening.

As YCC gave way to a FED backstop where the recycling ballooned

the Fed's Balance Sheet and Auction after failed Auctions began to

appear beginning at the long end of the Curve.

My Thesis proved 100% correct, then as now.

We anticipate a reaction to Mid Curve on today's ReCalc.

Safe Trading.

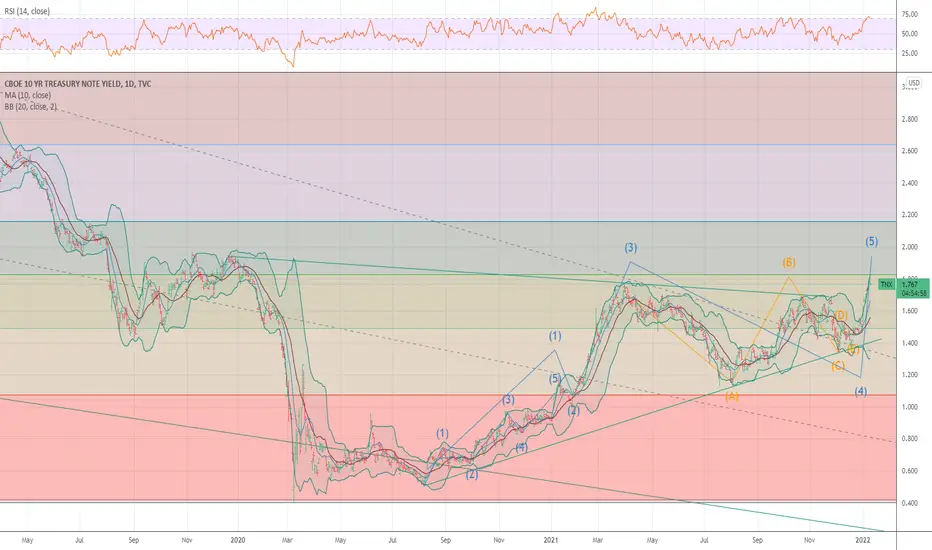

10yryields

10Y YIELD CRATERING SOON? EXTREME FEAR EXPECTED IN 1Q OF 2022Hello traders & investors!

As we look into the beginning of 2022 and use 10Y as our guide - expect enormous amount of fear coming to the markets/news channels/politician speeches..

I am expecting 40-50% correction on this 10 Year treasury. Cash will flow into bonds and DXY should strengthen at the same time too :)

That being said, I expect this to unfold in first half of 2022. Multi-year and decade long views does not change - rates will climb much faster & higher.

We have nice place to enter the markets in the times of extreme fear.

Levels to watch: 1.52% & 0.90%

Take care! This is not a financial advice.

10 yr yield to see 1.75 to 1.86 at 50% TOPPED The chart posted is that of the 10 yr yield A few months back my forecast was for a move backup to 1.75/ 1.86 into the 50% area . I stand by this being the TOP of the range and we are now set up for deflation to show up . the 10 year will not be moving up for sometime

10 Yr T Note Major Downside Target In this update we review the recent price action in the US 10Yr T-Note and identify the next high probability trade location and target

TNX - The Tech WreckerAs yields began another disorderly move, The NQ finally took notice.

The range posted for the NQ this Morning - Traded in Full.

It was nice to see Reality begin to sink in finally.

Industrial caught the spillage while the 711s were hammered with9ut

relenting.

____________________________________________________________

FOMC @ 2 PM EST tomorrow should set the Trend for some time to come.

Bonds have been providing clear indications of a mishap, in particular ZN.

TNX - ROC @ 2.43%10 Year Yields getting itchy once again.

2Yr - 10Yr worthy of observation.

Dot Plot - 2022 @ 1.125%

Page 4 - www.federalreserve.gov

ZN - 10 Year Note Futures / Monthly @ 20 Yrs / The Abyss of DEBTIt is often said by Quantity Theorists echoing, Milton Friedman - "Inflation is always and everywhere a monetary phenomenon.”

Conditions... matter, they change as does the "moneyness of money" - but you can't keep the Chicago School of Economic

mind poisoning down.

That could be why I didn't play with academia, it is a toxic sandbox wed to a beach at times. Polluting the incoming tides.

Friedman could not have imagined how awry his QT has been turned on its collective head.

Gold Bugs to this day, quote this - scores of times every single day. "Were Gold Priced in DEBT

it would be $250,000+"

No one cares, least of all Central Banks who Demonetized it but made it legal to own under Nixon.

You all swap fungibles for... Silver? A Weimar home? Taco Bell?

Good luck, it's a Tier 1 asset on the Books of Central Banks for a reason and trades at a varying rate as it always has.

Q of M clearly isn't tied to it and it's not chasing away Good Money for Bad any longer... those storied days passed very

long ago.

_____________________________________________________________________________________________________________

Money loses its purchasing power parity in a number of ways - not simply through more money chasing goods and services,

this is merely one-sided - "ceteris para bis" Jedi Mind Fuck at its finest.

Causation is always assumed from the money supply increase to price rises...a very basic truth, but ONLY a precondition

and not a fate acompli.

____________________________________________________________________________________________________________

The Fundamental causes of a general price inflation are still supply-side factors - for example, rises in wages or prices of factor input costs - which we see in the PMI data - to date not fully passed onto Consumes due to Supply-Side Shocks ) or demand-side ones - high demand causing price increases in markets.

The fatal flaw is QMT assumes an exogenous money world and the wrong direction of causality.

The contraction in Broad Money with a Credit Money System aka Bank Money is destroyed as people move to acquire CASH money

or what is perceived to be a CASH Equivalent.

_____________________________________________________________________________________________________________

Simply Put: Aged Theory is flawed beyond. Supply Side Cocktails and the Ingredients of the CREDIT MONEY Elixirs are quite

different than in 1963 Uncle Milty.

______________________________________________________________________________________________________________

Speaking of Credit (DEBT MONEY if you can al it that) the BOE recently raised rates.

China, faced with new lockdowns surrounding the - Credit Squeeze (TY to Shevchenko for the prod to dig in and determine WTF) .

Turns out 6 property developers including the "Grande" have deferred wages the CCP now says must be paid by the start of the

Lunar New Year, oh and... yer gonna need to pay $21.37 Billion in Bonds or default.

Sounds bad huh? Not remotely...

Back wages amount to $174.38 Billion, can't pay 'em?

Lock 'em down, which is precisely what the CCP is setting up to avoid immense Social upheaval.

______________________________________________________________________________________________________________

Are we seeing a trend appear?

We are indeed. Debt Defaults have been propped by Governments to stave off tragic Social disruptions.

Hardly a footstep in the direction of Trust for Journey of 1,000 miles to default.

S'ok China, yer not alone, we proudly stand with you, although we've been at tit longer on this turn, so we're

just better at wallpapering over it with Currency Seniorage.

Yaun / Renminbi - only one works inside and one outside.

Hmmm...

That could not possibly happen here in the US of A, could it?

Naw.

_____________________________________________________________________________________________________________

When you destroy the Moneyness of Money with it goes all attendant prior theory as well as the very thing used to bring

Money into Circulation @ Tier One - The BOND MARKETS.

Fractional Reserve Banking merely extends it to obscene levels of Leverage and DEBT which are far beyond repayment.

Toss in the 6% Vig the FED takes for this privilege and after a hundred or so years, they end up owning everything.

They are, after all, the lender of last resort, the DTC merely the record keeper for when the payments halt and DEBT

becomes unserviceable.

What are your opportunity costs to Debt?

What do you value?

Forget Price it's no longer a metric for the sane, merely a distended and starved stomach.

_____________________________________________________________________________________________________________

Moral:

When Risks are ignored, they are mispriced...

10 Year Note Yield - Short / Intermediate Duration

Inflation has been mispriced in excess of 16 months. The Federal Reserve should have

begin to reduce Liquidity by Mid 2020 as Fiscal Stimulus had taken effect into July into

September when Fiscal Stimulus began Peak.

The Fed's Balance Sheet continued to expand with the Purchase of RMBC/MBS/UST/Corp.

Debt, while Shadow operations under FASB 56 continued to increase nearly matching the

Fed's accumulated Holdings. $8 Trillion in combined Net exposures, provided outsized

gains for Equities.

Bonds began a revolt in early 2021, only to see the Fed step up and employ YCC in early

April, attempting to stem the fastest rising rates in US History.

The Fed and US Treasury can control all Points on the Yield Curve as the Buyer of last resort.

Clearly, the Short End used to require far less effort when re-fundings were under 30 Months.

This is no longer the case, as they expand funds from 5-7s out to the '30s where we have seen

multiple "Auction Failures". Buyers simply refused to participate.

A Creep effect begins to enter the equation with respect to expectations.

The Long End of the Curve begins to flatten, traditionally indicating a recession ahead according

to conventional Bond Wisdom. And therein is the issue, this is not the 1970s and StagFlation

is not the Environment.

We are within an Inflationary Depression and have been for some time by any real and

credible Metric.

Economic Activity began to lag in Q1 2021, by Q2 the results were Peak consumption for

the US Consumers. It will be downhill for into Q3 and worsening into Q4 as we indicated

in July, all metrics were showing clear signs of another Global Slowdown as occurred in

Q2/Q3 2019.

Excess Capacity was quietly, but quickly becoming underutilized, as well as under-reporting

of Global Economic prospects.

____________________________________________________________________________

For 2022, I see a rapid and substantive decline gaining Momentum.

Economic Activity was pulled forward into 2021.

Inflation Numbers need to be brought to heel with BLS Recalc for Inflation, taking effect

in January 2022. This extraordinary measure will fail. The headline Numbers adjusted by

this tampering will not change Prices Paid.

Malcontent - the result as What is purported and Reality will diverge to create further distrust

and increasing Loss of Confidence - Quickly compounding.

Quietly, absolutely not... as Monetary Policy will not be alone as the "Build Back Better" Fiscal

Policy has been delayed. Further Stimulus down the road... only serves to compound the problem

and stave off the Pitchforks and Lanterns.

_____________________________________________________________________________

Covid Variants continue to expand - 19/ Epsilon / Delta / Omicron / New Variant TBA

The Fed indicated in their most recent FOMC Meeting Minutes and Press Conference, Omicron

is an "Uncertainty" and why the FED called it out within their Policy Statement.

Indicating the US Economy could handle the "Omicron" Variant at present while acknowledging

the FED is a "Long Way from knowing what it will turn out to be..."

"It is unclear on how the New Variant would suppress Demand and Supply."

"Wave upon wave, people are learning to live with this..."

Vaccinations, according to the Raven reduce the "Economic Effect."

Timeline for Variant assessment - 3 to 6 Weeks... Omicron doesn't really have an impact on the

Taper as the Chair wants participants to believe.

_______________________________________________________________________________

The Stock Market is and is not the Economy - it depends on which way the wind is blowing. A

Northern Gale changes arrangements, this is what the Raven is laying the groundwork for into

Q1.

An overextended Credit based Financial Economy has a great number of hurdles ahead in addition

to a Central Bank which may or may not embark on further meddling.

That is immaterial to a larger extent as Global Markets for DEBT are Tightening at a time when

the compound effect of all Economic activity is waning... instructs us all as to how "intent" will

reprice DEBT / Inflation / Expectations and Sentiment.

__________________________________________________________________________________

Factors that lead to growth in 2021... the plug is being pulled.

Q4 rebound is a seasonal pattern, and yet Holiday sales will prove to have been DISMAL.

The Dollar remains at risk to the upside, clearly holding its own, the Dollar will move higher

at least to 100.

___________________________________________________________________________________

The Fed can do plod along - Markets will adjust as they permit the Net Drag to do their work for them.

___________________________________________________________________________________

Regional BAnks are showing two consecutive quarters of Savings Drawdown from Q3 thru Q4.

___________________________________________________________________________________

The Inflation/deflation debates have always amused me as an Economist. This is best framed within the

context of Credit Malfeasance again the expansion of Moore's Law to an Exponential Function.

Technology is deflationary, it reduces a great many Economic functions while increasing efficiencies

in ways, most fail to understand.

Monetary Policy is the Inflation component with an added twist, the Supply Shocks and shortages due

to the Shut Down of the Global Economy. An extraordinary time in Humanity's History.

This will be discussed at length in follow-on commentary.

_____________________________________________________________________________________

Moral hazards abound and are plentiful at precisely the wrong time.

A Nation of Gamblers - www.tradingview.com

PS. - the House always wins

10 Year Note Yield - 2%+ Ahead Into June - AugustThe Price Objective remains 2.28%.

Beyond sewing the usual seeds of discontent, observe the Larger Monthly Indications.

The above Chart is of extreme importance, it demonstrates how Capital Stocks begin to

turn, Glacial at first, as Momentum builds, they begin to accelerate.

This will end up a 4 or 5 part series discussing the potential impacts.

_____________________________________________________________________________

Price has broken above 2 Key Downtrends. It is attempting to reach the 3rd, which has acted

as resistance for years.

This is a material change in the underlying Bond Market Note Structure. It is no longer the

conventional depository for Principal and Coupon as a great many believe.

______________________________________________________________________________

Capital Stocks are in need of review:

Real Estate - the Hybrid / Principal and Coupon (Rents) A Negative correlation to Higher Rates

with cascading effects to Higher Rates. A 70% increase in Conventional and Jumbo Mortgage

Rates would see a 18 to 24% drop in the Price of Residential Real Estate.

Equities - the Buyback / Prop where Corporate Debt is used for Buybacks

Increased borrowing Costs temper Buybacks, Inflows do not. This is a double

edged sword we will discuss in detail.

Bitcoin - The repository (Not Depository) for excess Liquidity. BTC has a Positive

correlation to rising Rates. BTC has a Price Objective near $137K at the extreme

extensions for Rates of the 10 Year Note Yield.

Bills / Notes / Bonds / - Debt instruments with attendant Hybrid function of Principal / Coupon.

______________________________________________________________________________

Bonds (prior to 2006) were traditionally a function of the Business Cycle which has been supplanted

by the Credit Cycle (no longer a Cycle by appearances).

Prior to 2008 Congress would pass a Bill in the Legislature, after speaking with the US Treasury to

determine how to "Finance" its Fiscal requirements. Once the Bill was passed and signed into Law,

the US Treasury would conduct operations with the Federal Reserve Central Bank in New York to

issue the increased Credit/Debt (The FED taking their statutory 6% issuance) to the US Government.

Bills, Note and Bonds would be placed with Primary Broker Dealers (Fed Member Banks) and offered

at "Auction" to the Public, Institutions, exogenous Central Banks, Funds, Swaps and overnight Swaps

for shorter duration T-Bills sweeps.

This funding mechanism for DEBT no longer exists.

FASB 56 - took the Governments Budgets and Funding "Dark" as a "Matter of National Security". The

General Purpose Federal Financial Reports are Classified Documents.

The material Facts of FASB 56 - files.fasab.gov

13 Short Pages well worth educating one's self as to how the Government conducts itself.

TARP/TALF were undisclosed Operations which maintained their Shadow Financing for years.

94% of Americans were against Commercial Bank Bailouts. Privatizing Gains while publicly

subsidizing losses was viewed with extreme displeasure.

___________________________________________________________________________________

Over the past 14 Year, we see the outcome(s) - Interventions in Auctions by the Federal Reserve,

Yield Curve Control, the Outright Purchase of RMBS/MBS again (this began in 2004 in size as the

Federal Reserve's concerns over Real Estate began to mount).

The FED has become the buyer of Last Resort - currently @ $8.758 Trillion in Assets of which

$8.296 are "Securities" - this excludes "Shadow Operations" of FASB 56.

In less than 2 years, the Federal Reserves Balance Sheet rose from $4.212 Trillion to more than

Double that amount (NET of Shadow Operations)

I estimate Shadow Operation under FASB 56 to be in excess of $3.8 Trillion - this excludes the

Trillions missing from the Federal Coffers @ DOD, HUD and a great many other Agencies.

_________________________________________________________________________________

Follow - On commentary will begin breaking down the Trends and discuss the potent outcomes

and timeframes for each Capital Stock.

There is a large amount of information to be discussed, requiring a methodical analysis of

all points on the outcome curve.

More to follow - HK

TNX - Zimbabwe / YCC / Capital Stock / Melt Up / FX - ECB BOJ EUBonds are at a Critical Juncture.

Unable to serve their function due to YCC we are now

staring down the Crack the Boom Phase V.5

Not much is functioning correctly... not remotely.

_______________________________________________

We are quickly becoming Zimbabwe.

Of the 3 Capital Stocks, Equities may well end up the

catch-all bucket and Melt Up in Violent Fashion.

By appearances, the Equity Complex itself is the remaining

capital Stock for the Inflation Trade.

Real Estate is immobile, illiquid and the Bond Market

remains on the Path of Destruction. Both DOA in Real Terms.

If you did not believe this earlier, perhaps now...

The Raven has made it clear you will lose 2x as quickly.

Welcome to Zimmy World akin to Waterworld but we are

afloat in a Sea of Sharks feeding on the remaining viable,

liquid - Equity Complex.

McC OSC's are deeply in negative for all Indices - DEEP.

They declined yesterday as the ES NQ YM RTY all reversed.

Frankly, horrifying as What is, is not what should be as the

Flamingo's Sports Book has gone into DeFib Mode.

___________________________________________________

They are using the Recalc to extend and pretend, a concern

we expressed would be a game-changer, it now is realized.

Yes, the Indices are grossly overbought and could face a reversal...

Maybe...

A great deal will depend on how committed Everyone is to the

Zimbabwe Trade.

___________________________________________________

Sad, pathetic, destructive - yes.

It is what it is, be prepared for complete Insanity.

It's beginning.

Powell made it quite clear, repeatedly clear - the Focus and cover

is labor. Rates... the slide in 2 for 2022, lied, of course, then added

potentially 3, then mentioned 2024...

The FEDs #1 Mandate is Price Stability... # 2 Full Employment.

Raven went all in by not mentioning Mandate #1, they abandoned

it. It isn't Transitory - it is the way, Instability.

Both are now a joke so depressing, it warrants consideration

as to what they are truly after.

It is quite simple - protect their own.

It disgusts me to write this, but I'd be remiss in not doing so.

_____________________________________________________

The Only thing that can upend this insidious trend is Yields.

Flattering to Inversion on the Short End will take time.

Equity Complex Extensions to follow in Commentary.

TNX 10 yr. yields TNX so far in Dec. Ms1 pivot point to the MP. So far this quarter, Qr1 to QP. Institutional traders use pivot points.

TNX - Creating Issues

Set your Clock by it...

The 007s begin their Ghost Stories at Highs.

Within mere hours of our 2 favorites Bond Stand-Ins - Moore and Dalton.

TNX wakes up.

TLT drops $4.

Whenever Shevchenko and Dino begin another series of rants, it is a SELL.

The "Wood Paneling" Indicator has never failed.

It remains 100%.

__________________________________________________________________

Since July I have suggested there is no "Safety" Trade in Reality, for Bonds.

It remains hitched to prior paradigms.

For reasons, repeated enough times to not require further repetition, sanguine.

My heart says Michelada, but it's Sangria today.

___________________________________________________________________

The Federal Reserve remains the Ultimate Bagholder, their balance sheet continues

to Hold steady.

Why?

How come?

Wassup there?

There remains a need to Feed.

The FED is going to raise rates, accelerate the Taper to ~$30 Billion for MBS and UST's.

Ideally, they want to conclude the shortest Taper in History by March.

3 Rate Hikes are confirmed for 2022, a 4th in discussion as Forward Guidance on Inflation

is dismal... 20 to 25% for 2022 for starters.

______________________________________________________________________

The Answer is wrong again.

Unsure how mass delusions perform any longer as they have stretched my imagination beyond

what I considered sane, probable... possible, of course.

My mind has more stretch marks than my waist.

Remarkable times.

US 10Y Bonds...What Do We Know?TVC:US10Y

With the wild drops in the market over the last few weeks, I have considered turning a greater percentage of my portfolio to bonds. Listed in this article are the findings of my research.

Todays Yield closed at 1.341%, investors receive a coupon of $1.375 semi-annually. Wow...That is pretty discouraging. With insanely low interest rates this year, (Note interest rates and bond prices are inversely related), bonds are expensive for very little yield. The feds have released data on a 6.20% inflation rate which is rather naive in my opinion, considering they continue to print money. The M2 Money Supply measures the total cash and equivalents in the USA, this grows on average of 11.31% a year, we are at a YTD of about 37%. Over three times the average currency printed. This large money supply is a main factor in why interest rates are so low. So will interest rates ever grow back to their pre-COVID levels? That is not for me to answer, as I have no idea. I enjoyed a projection done by @RealMacro about how we are rapidly heading towards a recession. I believe all investors can agree that it is perfect market conditions for a recession. Many investors are very new; they have never experienced a recession, this has come from the meme stock phase. Will investors begin pouring into fixed securities? Is the security worth the expensive costs and low yield? Will the feds continue to purchase bonds back? It is important to note, when the Feds buy back bonds they are increasing the money supply in the economy by swapping bonds for cash, and opposite when selling bonds. If the Feds wanted to cut back inflation wouldn't it make sense to sell more bonds? But by cutting back interest rates, would investors really have an incentive to purchase bonds?

Key Notes:

M2 Money Supply Measures the total cash in circulation

Bond Buy Backs - Increase Money Supply

Bond Sell Offs - Decrease Money Supply

Money Supply and Interest Rates are inversely related

Bond Prices and Interest Rates are Inversely related

Bond Yields and Interest Rates are parallel

NOT INVESTMENT ADVICE - I am not a licensed Advisor

Critical AriasWave Market Update - Things Are Slowly Turning...In this video I lay out my preliminary analysis and thoughts as to why these markets will take a hit.

Based on AriasWave I will explain the kinds of trend changes we will see.

Some have already started turning and some are still in the process of doing so.

I recommend staying tuned as I will be starting to release these updates on a regular basis as required.

Remember to use Disciplined Money Management Principles to ensure longevity as a trader.

If you don't know the long term pattern shouldn't you be doing your research instead of just following the crowd?

Just remember: I am not a financial advisor, I suggest using this only as a guide. Always do your own research.

Yields, 15 Nov. Another Failed H&S Pattern?The 10-year yield has printed a failed H&S pattern. So it is worth looking at it from a technical perspective.

Geometry:

The H&S target at 1.380 was not reached, instead the yield climbed back above the neckline (blue dashed line). This is a small but important detail. A failed H&S pattern is often a strong continuation pattern.

Fractals:

The area marked in red shows the same scenario: A failed H&S with a large move up after consolidation below the neckline. Small patterns give us a hint about large patterns, because they reveal the personality of that instrument.

Elliott:

We are able to count a wave iv (in green) which is part of a larger wave (iii) in blue. This wave, in turn, may be part of a larger wave 1 or leading diagonal.

How I trade it:

Support on top of 1.500 would indicate that yields are ready to move higher. The pitchfork median can act as local resistance.

TNX - The Event we've been waiting for since July We have repeatedly indicated the "Everything Must Go Sale" would begin

once we saw 10 Year Note Yields Cross 1.645 and then move beyond 1.71

to 1.76 and onto 2.12%

All asset Classes being sold is NOT something the Majority of Investors

remotely understand or believe it possible.

Preferring Correlations and Inverse Correlations to remain the Norm.

It isn't and the September Sell-off appears to have been forgotten.

Not surprising, memories are short, convictions are strong.

Price does not care what you "believe" - rather it demonstrates the

convictions of your beliefs.

Belief in the 11X Bond Complex... remains at all-time highs.

Return of depreciating Captial is favored to Equities which continue

to be the perceived Inflation Hedge.

The circular Logic is a complete Sh_t Mix of Mass Delusions as participants

will discover one the Next Great Unwind begins.

Everyone losses a hand.

_______________________________________________________________

With last week's one Day Wonder spiking @ nearly 10% while the DX began

to move over 95... RCO's are again heating up.

_______________________________________________________________

We indicated the Infrastructure Bill would end up @ $1 Trillion after all

the non-sense - Ultimately it was the FEDs handlers who reduced the

increased threat of a Bond Market Accident.

Suggesting DC piddle into a far less Aggressive Final number, Rates were

tamed down, preventing an even larger protest from the 007s.

Monday, President Biden signs into Law - $ 1 Trillion Infrastructure Bill.

AKA - another Giveaway to Insiders.

_______________________________________________________________

How much time does this Buy for the Equity Complex, we shall see.

It will become yet another nail in Confidence Coffin as Inflation continues

to Beat Expectations.

_______________________________________________________________

Q4 begins to see squaring of Position for yeat end begin into December.

With Notional Bets to a Strong finish to 2021 for appearance's sake, there

IS something out there... that will blindside the markets.

_______________________________________________________________

The 30 Year Auctions Failure... did not go unnoticed.

TLT - ROCs @ Mid Curve007s have been back announcing the latest "Sure Thing"

in Scottish Moors.

Just bring back the Wood Paneling, please.

We would appreciate Steve leaving our Front Yard.

_______________________________________________

TLT has not closed over its recent Highs.

All Bets at the Flamingo's Roulette Wheel are on 33.

_______________________________________________

With the 2nd highest ROC in a few weeks @ +7.75%...

Sightings of "Wrong Way Conway" @ Gilligans Isle/

We'll Oppose - as when we hear Metal to Metal contact,

loud crunching sounds, glass breaking, blood, and bags

of Frito Lays strewn about...

Train Wreck.

10Y still holding support.The US10Y, most liquid instrument in the world still holding our Orange support lines with a probable

target of >2 the upper line of the channel. Any break for the Orange support/Red lines stock markets

could/might go into a bullish move just like 2000.

TNX - 10 Year Note YieldNo mention of the 2% jump off the Trend Line for Yields.

We sold TLT 3x today.

ZN, as indicated after the 8 AM Sell, provided the Direction.

The Equity Complex is setting up the Reversal with Squeeze

after Squeeze.

For the next 3 Trading Days - Continue to press all SELLS to 45%.

____________________________________________________

The Bond Market will call the FED again...

We anticipate a Chop into one Final High prior to a Sharp Reversal.

TNX - 10 Year Note YieldWaiting on ZN to break 130 again.

Rates up .9% this morning.

IF the FED panders to Equiites.

Bonds will sell, there was an 8 AM EST SELL

TNX - RSI remains above 50The 10 Year Note Yield, in prior downtrends would provide the RSI in the Negative well below 50.

ARCA, as always is used to Prop Up the FANG GANG.

But BANG, the die is cast.

Anticipating a reversal in the 10 Yr Yield into the FOMC, which creates and enforces the SELL in

TECH.

EPS, as indicated months ago, would be a complete disaster...

Delivered.

NQ ES YM - 4 Gaps below

Symmetry mirrors September 15, 2021 reversal setting up.

2% - 2.12% - 2.37% Price Objectives on Break of 1.765

TNX - MeanwhileWhile Higher Taxes for the Muddle Class are on the way.

The Billionaires Boys Club sees the Stimmy as their Salvation.

Higher Taxes? Only if I can get First Abuser Rights to 10X what

I'll be required to pay for "Them"....

The Bond Market believes the Stimulus - "Further Recovery,

Infrastructure, Spending Bill" will get things on track once

it's pared back to $1 Trillion...

How do you mend a Broken Global Economy as Yield Curves

are flattening around the Globe?

You cannot.

Global Markets - showing the way.

And all those people out of work and resources?

F_ck em, appears to be the Path.

____________________________________________________

Have a good evening everyone

Allocation to bonds fell to the lowest level ever !!!This is a key takeaway from the latest monthly fund manager survey, conducted in the week through Oct. 14. While the outlook for global growth turned negative for the first time since April 2020 and the overall survey was the least bullish in a year, the allocation to bonds fell to the lowest level ever as inflation woes drove expectations for higher rates, according to Michael Hartnett.